Top Reasons Homeowners Are Selling Their Houses Right Now

Some people believe there’s a group of homeowners who may be reluctant to sell their houses because they don’t want to lose the historically low mortgage rate they have on their current homes. You may even have the same hesitation if you’re thinking about selling your house.

Data shows that 51% of homeowners have a mortgage rate under 4% as of April this year. And while it’s true mortgage rates are higher than that right now, there are other non-financial factors to consider when it comes to making a move. In other words, your mortgage rate is important, but you may have other things going on in your life that make a move essential, regardless of where rates are today. As Jessica Lautz, Vice President of Demographics and Behavioral Insights at the National Association of Realtors (NAR), explains:

“Home sellers have historically moved when something in their lives changed – a new baby, a marriage, a divorce or a new job. . . .”

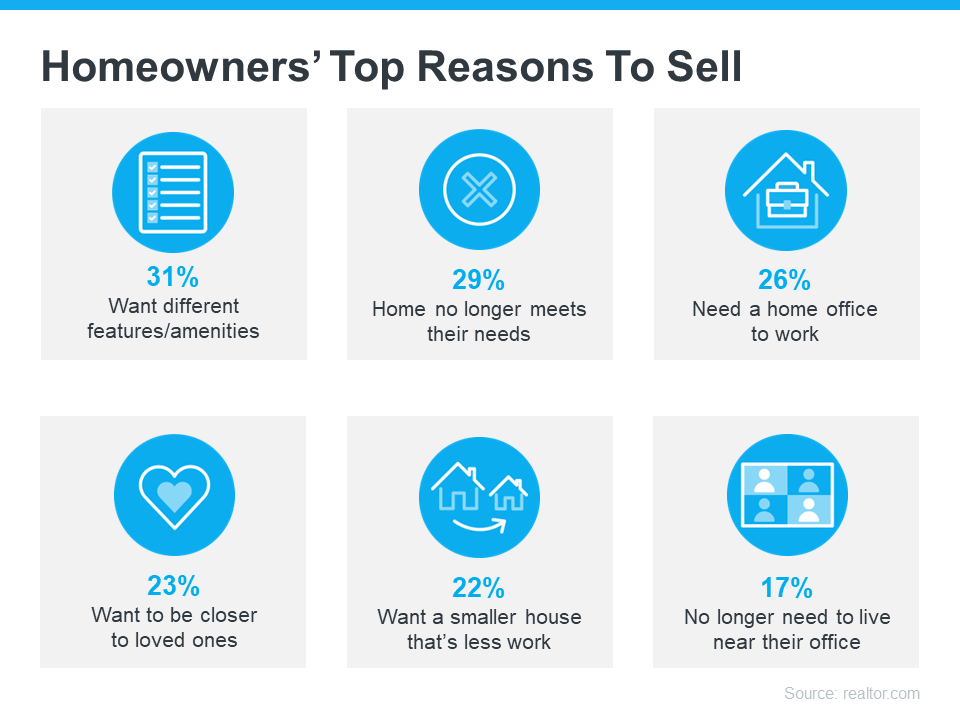

So, if you’re thinking about selling your house, it may help to explore the other reasons homeowners are choosing to make a move today. The 2022 Summer Sellers Survey by realtor.com asked recent home sellers why they decided to sell. The visual below breaks down how those homeowners responded:

As the visual shows, an appetite for different features or the fact that their current home could no longer meet their needs topped the list for recent sellers. Additionally, remote work and whether or not they need a home office or are tied to a specific physical office location also factored in, as did the desire to live close to their loved ones.

The realtor.com survey summarizes the findings like this:

“The primary reason homeowners decided to sell in the last year was the realization that, after so much time spent at home, they wanted different features and amenities, such as walkability, outdoor space, pool, etc. . . . ”

If you, like the homeowners they surveyed, find yourself wanting features, space, or amenities your current home just can’t provide, it may be time to consider listing your house for sale.

Even with today’s mortgage rates, your lifestyle needs may be enough to motivate you to make a change. The best way to find out what’s right for you is to partner with a trusted real estate professional who can provide expert guidance and advice throughout the process. They can help walk you through your options, so you can make a confident decision based on what matters most to you and your loved ones.

Bottom Line

While the financial reasons for moving are important, there’s often far more to consider. Non-financial reasons can also be a significant motivating factor. If you need help weighing the pros and cons of selling your house, let’s connect today.

What Sellers Need To Know in Today’s Housing Market

If you’re thinking about selling your house, you may have heard about the housing market slowing down in recent months. While it’s still a sellers’ market, the peak frenzy the market saw over the past two years has cooled some. If you’re asking yourself if you’ve missed your chance to sell your house and make a move, the good news is you haven’t – motivated buyers are still out there. But you do need to price your house right for today’s market. Here’s why.

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Homes priced right are selling very quickly, but homes priced too high are deterring prospective buyers.”

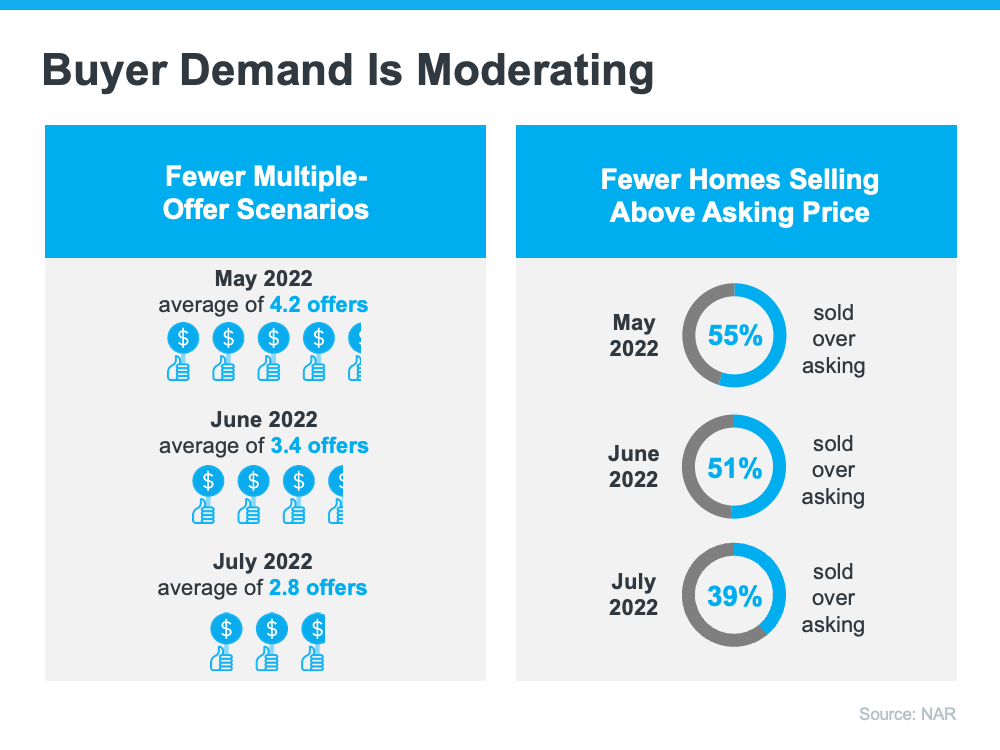

It’s true buyer demand has slowed over the past few months as higher mortgage rates made it more expensive to buy a home. The result is fewer bidding wars and less competition among buyers (see visual below):

But don’t forget – that’s compared to the severely overheated market we saw over the past two years. According to the latest Confidence Index from NAR:

“. . . 39% of homes sold above list price, down from 51% a month ago and 50% a year ago.”

While this is a slower pace than even one month ago, serious buyers are still in the market, and they’re buying homes that are priced right. In fact, the Confidence Index also notes the average home is selling in just 14 days.

If you’re aiming to sell your house, be sure you’re working with your agent to price it for today’s housing market. As buyer demand softens, it’s important to understand this isn’t the same market as last year. It’s not even the same market as just a few months ago. But it is still a sellers’ market.

If you’re ready to sell your house, seek the advice of a real estate professional. In some cases, you’ll need to adjust your expectations accordingly to meet the market where it is today. Selma Hepp, Interim Lead, Deputy Chief Economist at CoreLogic, explains what’s happening and what it means when you sell:

“Signs of a broader slowdown in the housing market are evident, . . . This is in line with our previous expectations and given the notable cooling of buyer demand due to higher mortgage rates. . . . Nevertheless, buyers still remain interested, which is keeping the market competitive — particularly for attractive homes that are properly priced.”

Bottom Line

While the housing market has cooled from its overheated frenzy, it’s still a sellers’ market. Let’s connect so you understand what’s happening with buyer demand and home prices in our local area as you get ready to enter the market.

What’s Causing Ongoing Home Price Appreciation?

If you’re thinking about making a move, you probably want to know what’s going to happen to home prices for the rest of the year. While experts say price growth will moderate due to the shifting market, ongoing appreciation is expected. That means home prices won’t fall. Here’s a look at two key reasons experts forecast continued price growth: supply and demand.

While Growing, Housing Supply Is Still Low

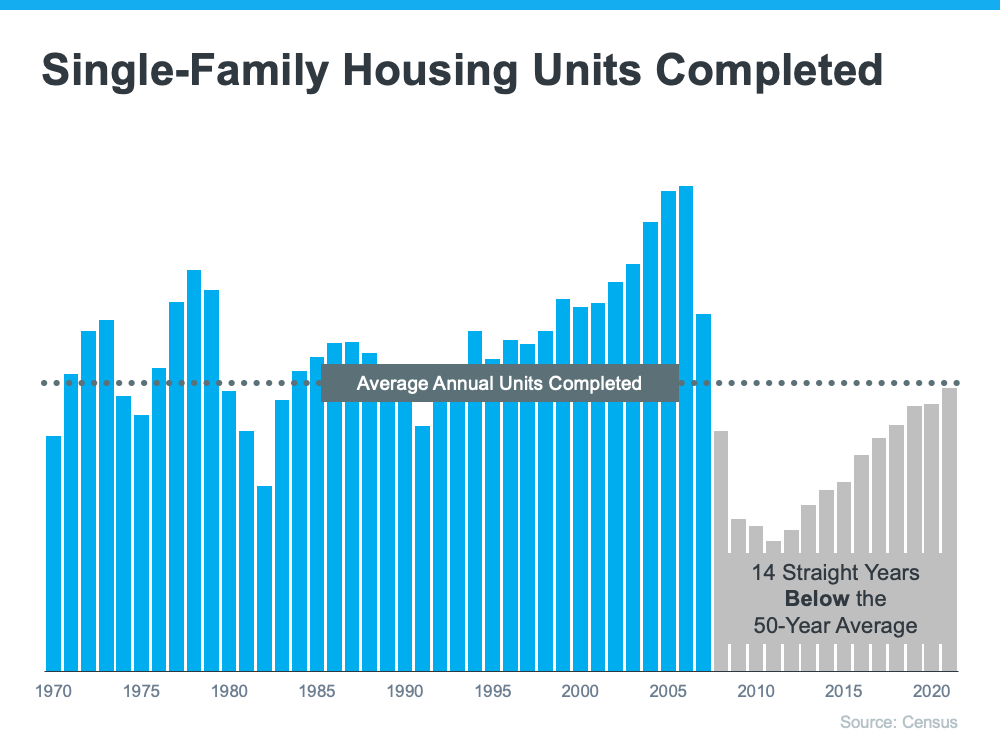

Even though inventory is increasing this year as the market moderates, supply is still low. The graph below helps tell the story of why there still aren’t enough homes on the market today. It uses data from the Census to show the number of single-family homes that were built in this country going all the way back to the 1970s.

The blue bars represent the years leading up to the housing crisis in 2008. As the graph shows, right before the crash, homebuilding increased significantly. That’s because buyer demand was so high due to loose lending standards that enabled more people to qualify for a home loan.

The resulting oversupply of homes for sale led to prices dropping during the crash and some builders leaving the industry or closing their businesses – and that led to a long period of underbuilding of new homes. And even as more new homes are constructed this year and in the years ahead, this isn’t something that can be resolved overnight. It’ll take time to build enough homes to meet the deficit of underbuilding that took place over the past 14 years.

Millennials Will Create Sustained Buyer Demand Moving Forward

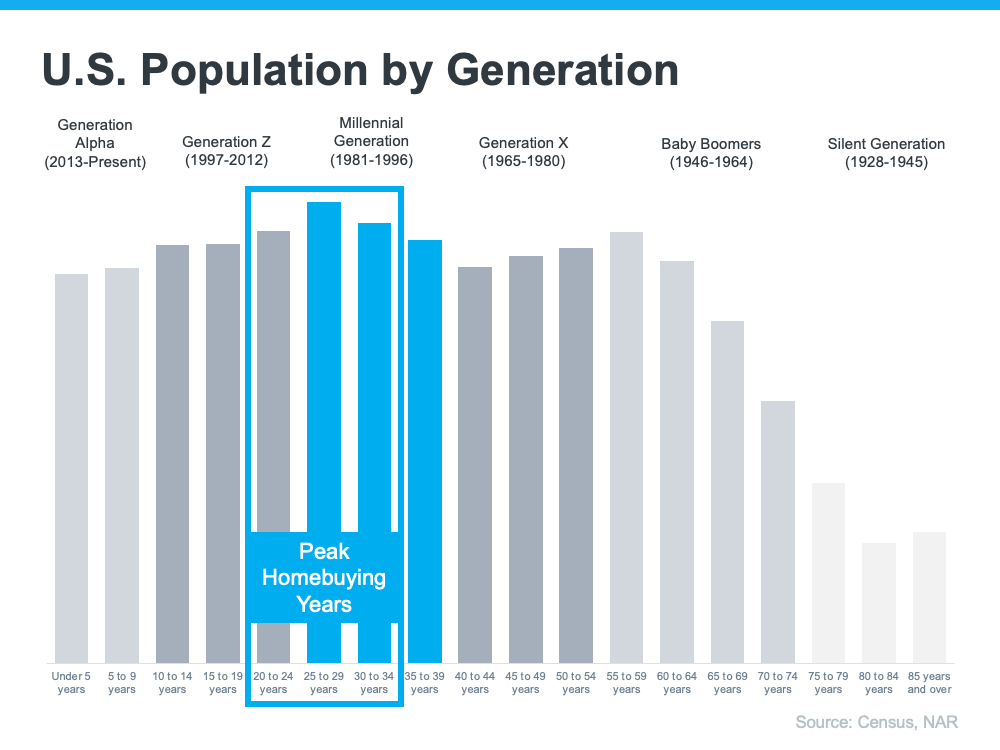

The frenzy the market saw during the pandemic is because there was more demand than homes for sale. That drove home prices up as buyers competed with one another for available homes. And while buyer demand has moderated today in response to higher mortgage rates, data tells us demand will continue to be driven by the large generation of millennials aging into their peak homebuying years (see graph below):

Odeta Kushi, Deputy Chief Economist at First American, explains:

“. . . millennials continue to transition to their prime home-buying age and will remain the driving force in potential homeownership demand in the years ahead.”

That combination of millennial demand and low housing supply continues to put upward pressure on home prices. As Bankrate says:

“After all, supplies of homes for sale remain near record lows. And while a jump in mortgage rates has dampened demand somewhat, demand still outpaces supply, thanks to a combination of little new construction and strong household formation by large numbers of millennials.”

What This Means for Home Prices

If you’re worried home values will fall, rest assured that experts forecast ongoing home price appreciation thanks to the lingering imbalance of supply and demand. That means home prices won’t decline.

Bottom Line

Based on today’s factors driving supply and demand, experts project home price appreciation will continue. It’ll just happen at a more moderate pace as the housing market continues its shift back toward pre-pandemic levels.

Homeownership Could Be in Reach with Down Payment Assistance Programs

A recent survey from Bankrate asks prospective buyers to identify the biggest obstacles in their homebuying journey. It found that 36% of those polled said saving for a down payment is one of their primary hurdles to buying a home.

If you feel the same way, the good news is there are many down payment assistance programs available that can help you achieve your homeownership goals. The key is understanding where to look and learning what options are available. Here’s some information that can help you.

You Can Qualify Even if You’ve Purchased a Home Before

There are several misconceptions about down payment assistance programs. For starters, many people believe there’s only assistance available for first-time homebuyers. While first-time buyers have many options to explore, repeat buyers have some, too. According to the latest Homeownership Program Index from downpaymentresource.com:

“It is a common misconception that homebuyer assistance is only available to first-time homebuyers, however, 38% of homebuyer assistance programs in Q1 2022 did not have a first-time homebuyer requirement.”

That means repeat buyers could qualify for over one-third of the assistance programs available. And if you’re a repeat buyer, you may still be able to take advantage of some first-time homebuyer programs, depending on your personal situation. That’s because downpaymentresource.com also notes many of the first-time homebuyer programs use the U.S. Department of Housing and Urban Development’s definition of a first-time homebuyer. Under their definition, you could qualify as a first-time buyer if you’re:

- Someone who hasn’t owned a primary residence in 3 years.

- A single parent who’s only ever owned a home with a former spouse.

That means no matter where you are in your homeownership journey, there could be an option available for you.

You May Be Eligible for Programs Based on Your Location or Profession

In addition to broader options available for repeat and first-time homebuyers, there are other types of down payment assistance programs that you could qualify for based on your location. According to the National Association of Realtors (NAR):

“Many local governments and non-profit organizations offer down-payment assistance grants and loans, targeted to area borrowers and often with specific borrower requirements.”

Plus, there are programs and special benefits for individuals working in certain professions or with unique statuses, including teachers, doctors and nurses, and veterans.

Ultimately, that means there are many federal, state, and local programs available for you to explore. The best way to do that is to connect with a local real estate professional and your lender to learn more about what’s available in your area.

Bottom Line

Down payment assistance programs have helped many homebuyers achieve their dreams, and if you qualify, they could help you too. Let’s connect today so you can begin exploring your options.

Sellers Have an Opportunity with Today’s Home Prices

As mortgage rates started to rise this year, many homeowners began to wonder if the value of their homes would fall. Here’s the good news. Historically, when mortgage rates rise by a percentage point or more, home values continue to appreciate. The latest data on home prices seems to confirm that trend.

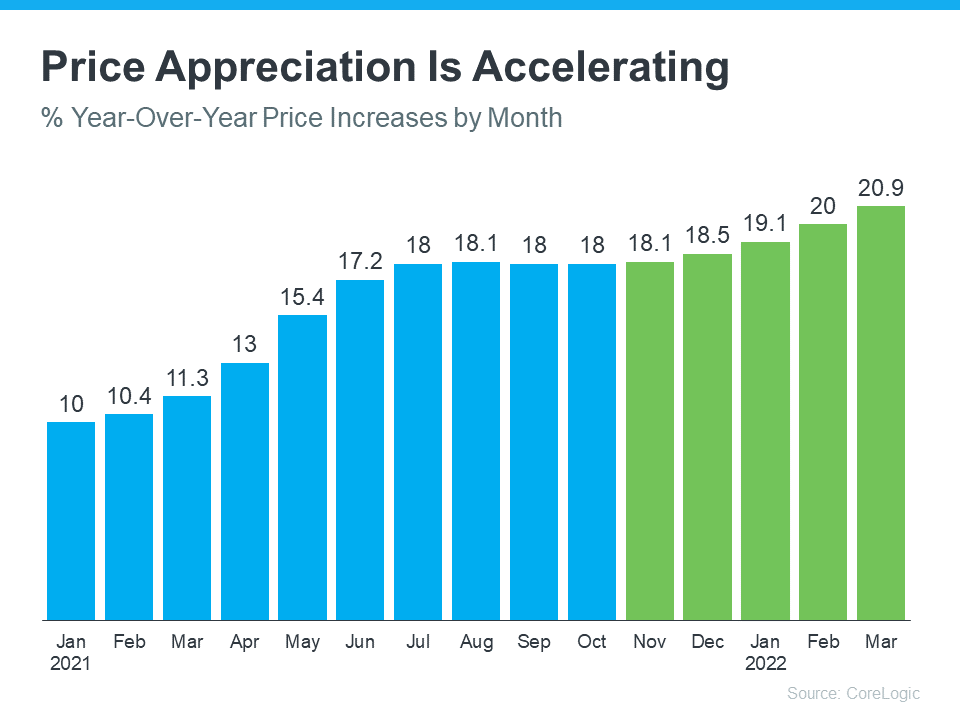

According to data from CoreLogic, home price appreciation has been re-accelerating since November. The graph below shows this increase in home price appreciation in green:

This is largely due to an ongoing imbalance in supply and demand. Specifically, housing supply is still low, and demand is high. As mortgage rates started to rise this year, many homebuyers rushed to make their purchases before those rates could climb higher. The increased competition drove home prices up even more. Selma Hepp, Deputy Chief Economist at CoreLogic, explains:

“Home price growth continued to gain speed in early spring, as eager buyers tried to get in front of the mortgage rate surge.”

And experts say prices are forecast to continue appreciating, just at a more moderate pace moving forward. A recent article from Fortune says:

“. . . the swift move up in mortgage rates . . . doesn’t mean home prices are about to crash. In fact, every major real estate firm with a publicly released forecast model . . . still predicts home prices will climb further this year.”

What This Means for You

If you’re thinking about selling your house, you should know you have a great opportunity to list your home and capitalize on today’s home price appreciation. As prices rise, so does the value of your home, which gives your equity a big boost.

When you sell, you can use that equity toward the purchase of your next home. And at today’s record-level of appreciation, that equity may be enough to cover some (if not all) of your down payment.

Bottom Line

History shows rising mortgage rates have not had a negative impact on home prices. Now is still a great time to sell your house thanks to ongoing price appreciation. When you’re ready to find out how much equity you have in your current home and what’s happening with home prices in your local area, let’s connect.

What You Need To Know About Selling in a Sellers’ Market

Even if you haven’t been following real estate news, you’ve likely heard about the current sellers’ market. That’s because there’s a lot of talk about how strong market conditions are for people who want to sell their houses. But if you’re thinking about listing your house, you probably want to know: what does being in a sellers’ market really mean?

What Is a Sellers’ Market?

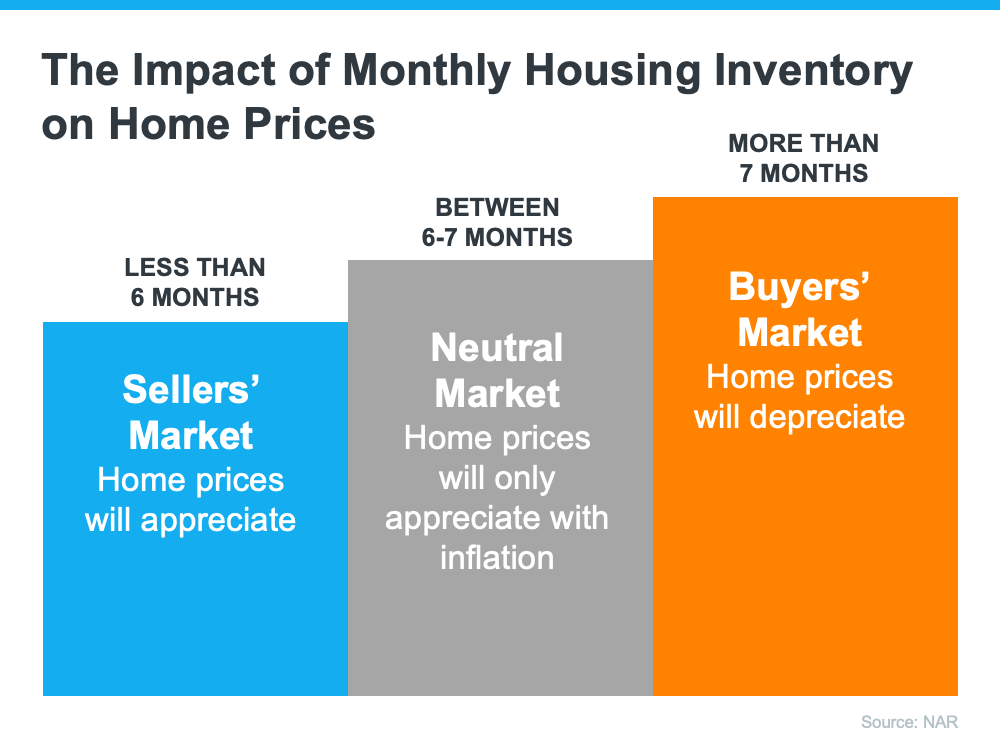

The latest Existing Home Sales Report from the National Association of Realtors (NAR) shows housing supply is still very low. There’s a 2-month supply of homes at the current sales pace.

Historically, a 6-month supply is necessary for a normal or neutral market where there are enough homes available for active buyers. That puts today deep in sellers’ market territory (see graph below):

What Does This Mean for You When You Sell?

When the supply of houses for sale is as low as it is right now, it’s much harder for buyers to find homes to purchase. That creates increased competition among purchasers which can lead to more bidding wars. And if buyers know they may be entering a bidding war, they’re going to do their best to submit a very attractive offer upfront. This could drive the final price of your house up.

And because mortgage rates and home prices are climbing, serious buyers are motivated to make their purchase soon, before those two things rise further. That means, if you put your house on the market while supply is still low, it will likely get a lot of attention from competitive buyers. Setting you up to be in a great position to cash in on all that added equity your home has been gaining!

Bottom Line

The current real estate market has incredible opportunities for homeowners looking to make a move. Listing your house this season means you’ll be in front of serious buyers who are ready to buy. Let’s connect so you can jumpstart the selling process.

What You Can Expect from the Spring Housing Market

As the spring housing market kicks off, you likely want to know what you can expect this season when it comes to buying or selling a house. While there are multiple factors causing some uncertainty, including the conflict overseas, rising inflation, and the first-rate increase from the Federal Reserve in over three years — the housing market seems to be relatively immune.

Here’s a look at what experts say you can expect this spring.

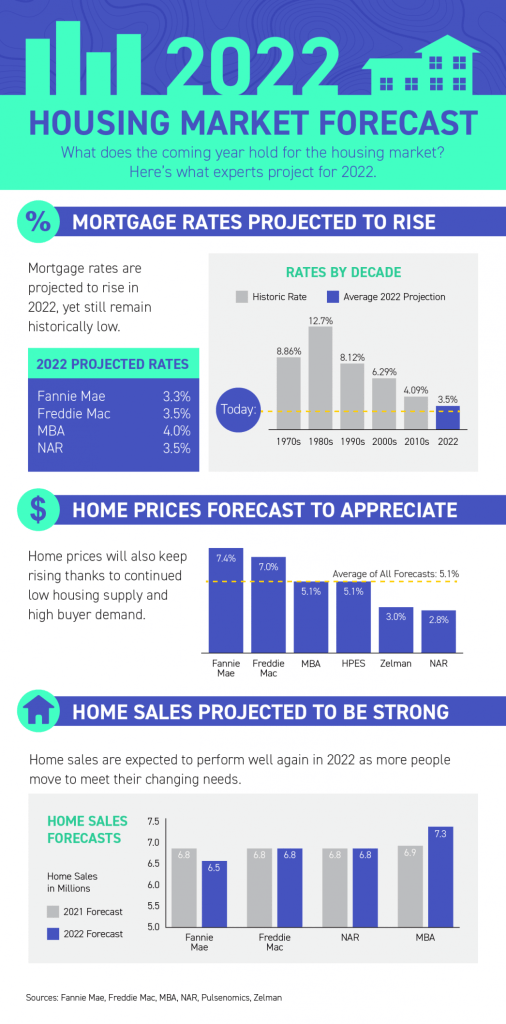

1. Mortgage Rates Will Climb

Freddie Mac reports the 30-year fixed mortgage rate has increased by more than a full point in the past six months. And despite some mild fluctuation in recent weeks, experts believe rates will continue to edge up over the next 90 days. As Freddie Mac says:

“The Federal Reserve raising short-term rates and signaling further increases means mortgage rates should continue to rise over the course of the year.”

If you’re a first-time buyer or a seller thinking of moving to a home that better fits your needs, realize that waiting will likely mean you’ll pay a higher mortgage rate on your purchase. And that higher rate drives up your monthly payment and can really add up over the life of your loan.

2. Housing Inventory Will Increase

There may be some relief coming for buyers searching for a home to purchase. Realtor.com recently reported that the number of newly listed homes has grown in each of the last two months. Also, the National Association of Realtors (NAR) just announced the months’ supply of inventory increased for the first time in eight months. The inventory of existing homes usually grows every spring, and it seems, based on recent activity, the next 90 days could bring more listings to the market.

If you’re a buyer who has been frustrated with the limited supply of homes available for sale, it looks like you could find some relief this spring. However, be prepared to act quickly if you find the right home.

If you’re a seller, listing now instead of waiting for this additional competition to hit the market makes sense. Your leverage in any negotiation during the sale will be impacted as additional homes come to market.

3. Home Prices Will Rise

Prices are always determined by supply and demand. Though the number of homes entering the market is increasing, buyer demand remains very strong. As realtor.com explains in their most recent Housing Report:

“During the final two weeks of the month, more new sellers entered the market than during the same time last year. . . . However, with 5.8 million new homes missing from the market and millions of millennials at first-time buying ages, housing supply faces a long road to catching up with demand.”

What does that mean for you? With the demand for housing still outpacing supply, home prices will continue to appreciate. Many experts believe the level of appreciation will decelerate from the high double-digit levels we’ve seen over the last two years. That means prices will continue to climb, just at a more moderate pace. Most experts are predicting home prices will not depreciate.

Won’t Increasing Mortgage Rates Cause Home Prices To Fall?

While some people may believe a 1% increase in mortgage rates will impact demand so dramatically that home prices will have to fall, experts say otherwise. Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae, says:

“What I will caution against is making the inference that interest rates have a direct impact on house prices. That is not true.”

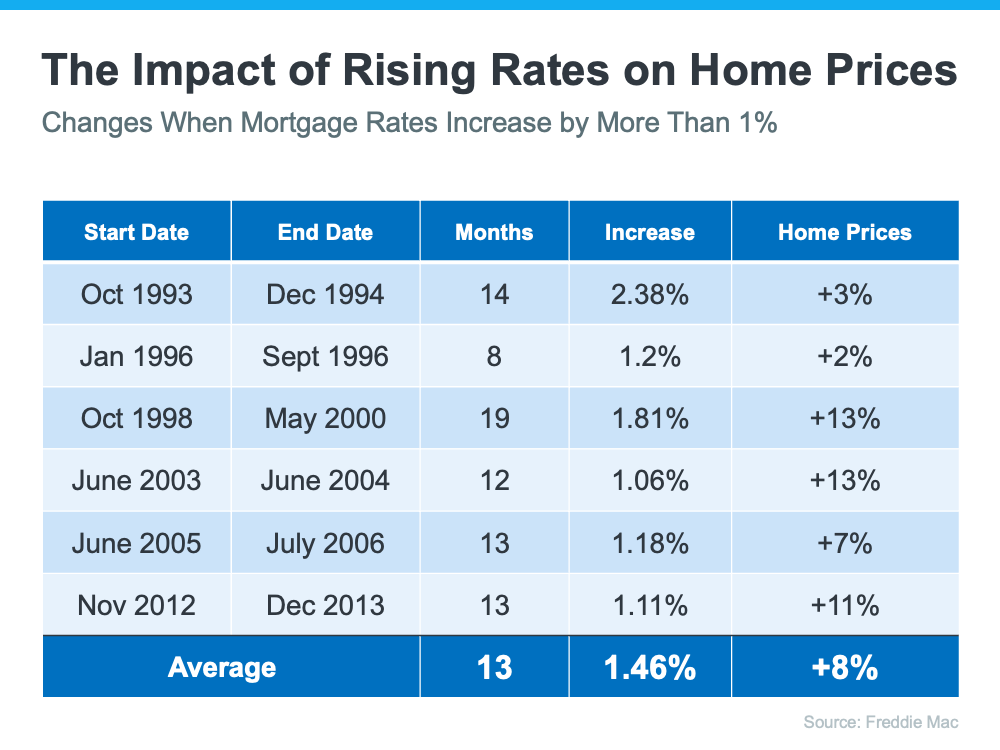

Freddie Mac studied the impact that mortgage rates increasing by at least 1% has had on home prices in the past. Here are the results of that study:

As the chart shows, mortgage rates jumped by at least 1% six times in the last thirty years. In each case, home values increased. So again, if you’re a first-time buyer or a repeat buyer, waiting to buy likely means you’ll pay more for your home later in the year (as compared to its current value).

Bottom Line

There are three things that seem certain going into the spring housing market:

- Mortgage rates will continue to rise – but it’s predicted to do so slowly and not dramatically.

- The selection of homes available for sale will modestly improve. Meaning sellers should get listed now to get the best deal possible on the sale of their home, and buyers should be ready to pounce on their dream homes quickly.

- Home prices will continue to appreciate, just at a slightly slower pace

If you’re thinking of buying, act now before mortgage rates and home prices increase further. If you’re thinking of selling, your best bet may be to sell soon so you can beat the increase in competition that’s about to come to market. Contact me today, to discuss your real estate needs & I will get to work for you!

Have questions, or want to discuss your goals, but would rather get started via email? Feel free to ask questions or let me know if you are looking to buy or sell using the contact form below & I will get in touch with you as soon as possible. If you would prefer that I give you a call, please include your phone number.

I look forward to working with you!

Expert Insights on the 2022 Housing Market

As we move into 2022, both buyers and sellers are wondering, what’s next? Will there be more homes available to buy? Will prices keep climbing? How high will mortgage rates go? For the answer to those questions and more, we turn to the experts. Here’s a look at what they say we can expect in 2022.

Odeta Kushi, Deputy Chief Economist, First American:

“Consensus forecasts put rates at about 3.7% by the end of next year. So, that’s still historically low, but certainly higher than they are today.”

Danielle Hale, Chief Economist, realtor.com:

“Affordability will increasingly be a challenge as interest rates and prices rise, but remote work may expand search areas and enable younger buyers to find their first homes sooner than they might have otherwise. And with more than 45 million millennials within the prime first-time buying ages of 26-35 heading into 2022, we expect the market to remain competitive.”

Lawrence Yun, Chief Economist, National Association of Realtors (NAR):

“With more housing inventory to hit the market, the intense multiple offers will start to ease. Home prices will continue to rise but at a slower pace.”

George Ratiu, Manager of Economic Research, realtor.com:

“We also expect a growing number of homeowners to bring properties to market, taking some pressure off high prices and offering buyers more options.”

Mark Fleming, Chief Economist, First American:

“Strong demographic demand will continue to act as the wind in the housing market’s sails.”

What Does This Mean for Buyers?

Hope is on the horizon for 2022. You should see your options grow as more homes are listed and some of the peak intensity of buyer competition starts to ease. Just remember, rising rates and prices are a great motivator for you to find the home of your dreams sooner rather than later so you can buy while today’s affordability is still in your favor.

What Does This Mean for Sellers?

Make no mistake – this sellers’ market will remain in 2022 as home prices are projected to continue climbing, just at a more moderate pace. Selling your house while buyer demand is so high will truly put you in the driver’s seat. But don’t wait too long. With more listings projected to become available, your ideal window of opportunity to stand out from the crowd won’t last forever. Work with an agent who knows your local market and current inventory conditions to ensure you have the support you need to make an educated and informed decision about selling in the coming year.

Bottom Line

If you’re thinking of buying or selling, 2022 may be your year. Let’s connect to discuss your goals and the unique opportunities you have in today’s housing market.

As Home Equity Rises, So Does Your Wealth

Homeownership is still a crucial part of the American dream. For those people who own a home (and those looking to buy one), it’s clear that being a homeowner has considerable benefits both emotionally and financially. In addition to long-term stability, buying a home is one of the best ways to increase your net worth. This boost to your wealth comes in the form of equity.

Equity is the difference between what you owe on the home and its market value based on factors like price appreciation.

The best thing about equity is that it often grows without you even realizing it, especially in a sellers’ market like we’re in now. In today’s real estate market, the combination of low housing supply and high buyer demand is driving home values up. This is giving homeowners a significant equity boost.

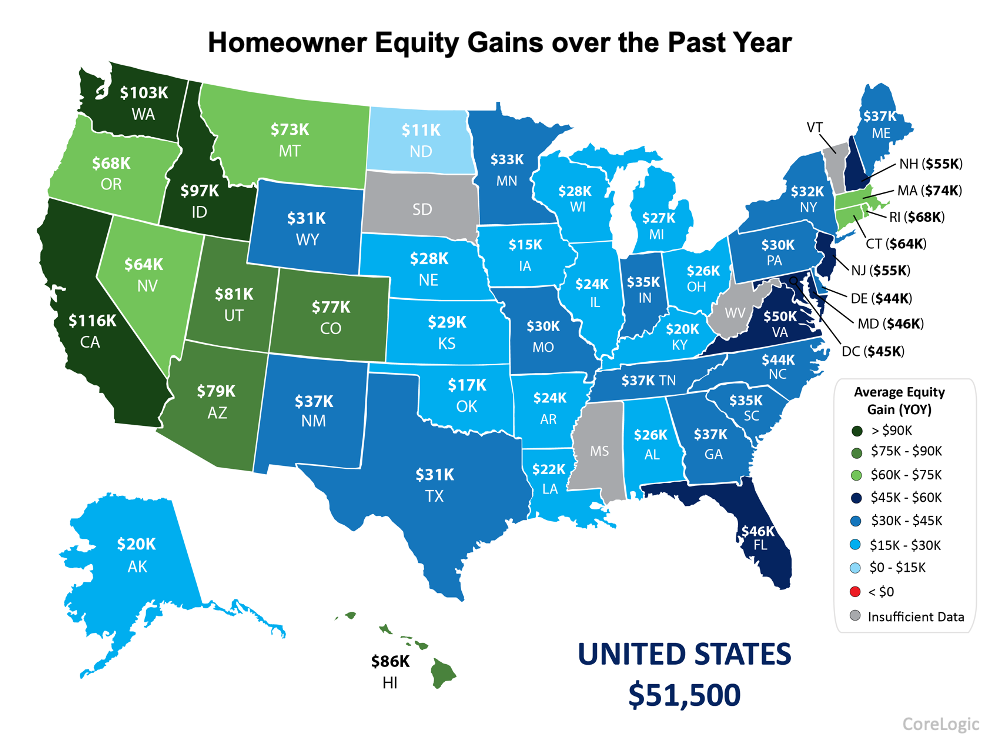

According to the latest data from CoreLogic, the amount of equity homeowners have has continued to grow as home values appreciate. Here are some key takeaways from the Homeowner Equity Insights Report:

- The average homeowner gained $51,500 in equity over the past year

- There was a 29.3% increase in national homeowner equity year over year

To give you an idea of what that looks like in your area, the map below shows the average equity gains by state.

What does all of that mean for you?

If you’re already a homeowner, you likely have more equity in your house than you realize. The numbers in the map above reflect year-over-year growth. If you’ve been in your home for longer than a year, you’ll likely have even more equity than that. That equity can take you places. You can use the equity you’ve gained to fuel your next move, achieve other life goals, and more.

On the other hand, if you haven’t purchased a home yet, understanding equity can help you realize why homeownership is a worthwhile goal. Homeowners across the nation gained an average of over $50,000 in equity this year. Don’t miss out on this chance to grow your net worth.

Bottom Line

If you want to learn more, let’s connect. I can help you understand where home prices are today, how they contribute to a homeowner’s net worth, and the impact equity can have when you own a home.

Contact me today to start the process of capitalizing on your homes equity or starting to build it by becoming a homeowner!

CALL (517) 643-1834 or EMAIL: morgan@morganrobinson.org

The housing market is prime for both buyers & sellers alike!

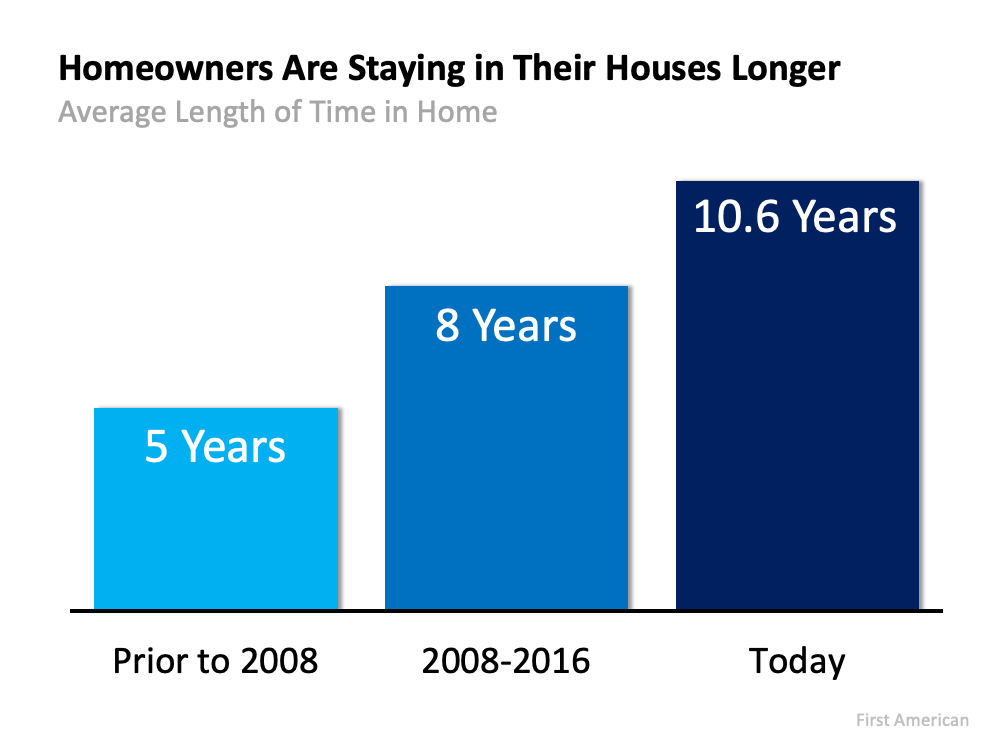

If you’ve been in your home for longer than five years, you’re not alone. According to recent data from First American, homeowners are staying put much longer than historical averages (see graph below):

As the graph shows, before 2008, homeowners sold their houses after an average of just five years. Today, that number has more than doubled to over 10 years. The housing industry refers to this as your tenure.

To really explore tenure, it’s important to understand what drives people to make a move. An article from The Balance explores some of the primary reasons individuals choose to sell their houses. It says:

“People who move for home-related reasons might need a larger home or a house that better fits their needs, . . . Financial reasons for moving include wanting a nicer home, moving to a newer home to avoid making repairs on the old one, or cashing in on existing equity.”

If you’ve been in your home for longer than the norm, chances are you’re putting off addressing one, if not several, of the reasons other individuals choose to move. If this sounds like you, here are a few things to consider:

If your needs have changed, it may be time to re-evaluate your home.

As the past year has shown, our needs can change rapidly. That means the longer you’ve been in your home, the more likely it is your needs have evolved. The Balance notes several personal factors that could lead to your home no longer meeting your needs, including relationship and job changes.

For example, many workers recently found out they’ll be working remotely indefinitely. If that’s the case for you, you may need more space for a dedicated home office. Other homeowners choose to sell because the number of people living under their roof changes. Now more than ever, we’re spending more and more time at home. As you do, consider if your home really delivers on what you need moving forward.

It’s often financially beneficial to sell your house and move.

One of the biggest benefits of homeownership is the equity your home builds over time. If you’ve been in your house for several years, you may not realize how much equity you have. According to the latest Homeowner Equity Report from CoreLogic, homeowners gained an average of $33,400 in equity over the past year.

That equity, plus today’s low mortgage rates, can fuel a major upgrade when you sell your home and purchase a new one. Or, if you’re looking to downsize, your equity can help provide a larger down payment and lower your monthly payments over the life of your next loan. No matter what, there are significant financial benefits to selling in today’ s market.

Bottom Line

If you’re looking to maximize your sale and minimize your effort, you need to work with a real estate professional. like me! In a housing market like today’s, it can be tempting to list your house on your own – known as For Sale By Owner (FSBO). But the truth is, a real estate professional can save you time and money by managing every step of the process, from pricing your home to reviewing documents and handling negotiations.

Contact me today, to get the ball rolling in the right direction, to maximize your sale & harness your purchasing power, whilst minamizing your effort in the process!