3 Must-Do’s When Selling Your House in 2024

If one of the goals on your list is selling your house and making a move this year, you’re likely juggling a mix of excitement about what’s ahead and feeling a little sentimental about your current home.

A great way to balance those emotions and make sure you’re confident in your decision is to keep these three best practices in mind when you’re ready to sell.

1. Price Your Home Right

The housing market shifted in 2023 as mortgage rates rose and home price appreciation started to normalize once again. As a seller, you still need to recognize how important it is to price your house appropriately based on where the market is today. Hannah Jones, Economic Research Analyst for Realtor.com, explains:

“Sellers need to become familiar with their local market and work closely with a local agent to make sure their listing is attractive to buyers. Buyers feeling the pressure of affordability are likely to be pickier, so a well-priced, well-maintained home is the ticket to drumming up big demand.”

If you price your house too high, you run the risk of deterring buyers. And if you go too low, you’re leaving money on the table. An experienced real estate agent can help determine what your ideal asking price should be, so your house moves quickly and for top dollar.

2. Keep Your Emotions in Check

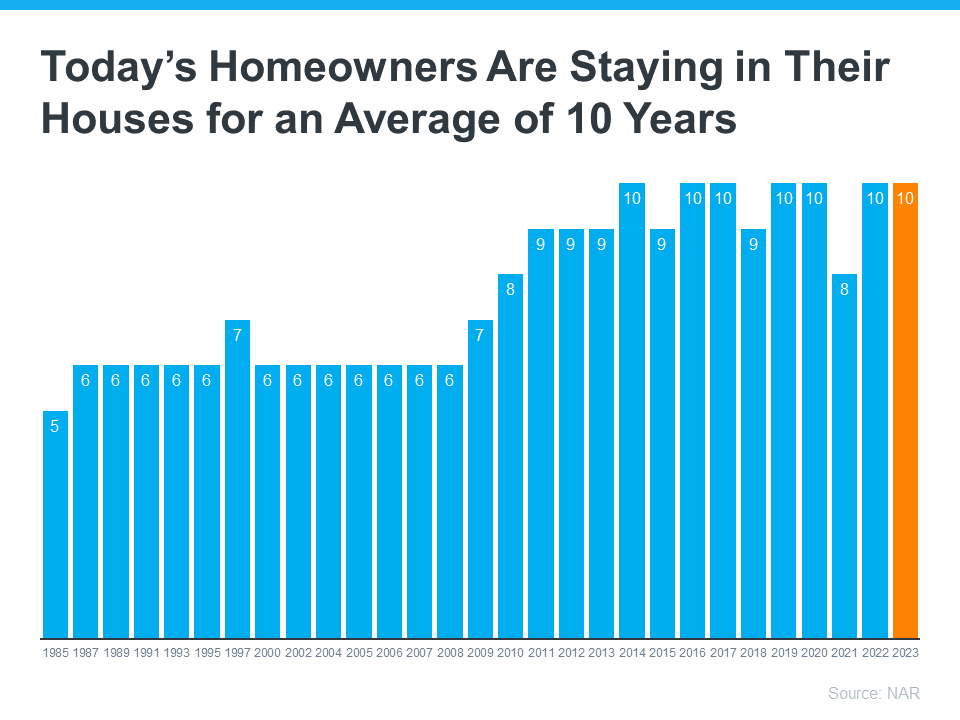

Today, homeowners are staying in their houses longer than they used to. According to the National Association of Realtors (NAR), since 1985, the average time a homeowner has owned their home has increased from 6 to 10 years (see graph below):

This is much more than what used to be the norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you bought or the house where your loved ones grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from the sentimental value.

For some homeowners, that makes it even tougher to separate the emotional value of the house from fair market price. That’s why you need a real estate professional to help you with the negotiations and the best pricing strategy along the way. Trust the professionals who have your best interests in mind.

3. Stage Your Home Properly

While you may love your decor and how you’ve customized your house over the years, not all buyers will feel the same way about your vibe. That’s why it’s so important to make sure you focus on your home’s first impression, so it appeals to as many buyers as possible.

Buyers want to be able to picture themselves in the home. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. As Jessica Lautz, Deputy Chief Economist and Vice President of Research at NAR, says:

“Buyers want to easily envision themselves within a new home and home staging is a way to showcase the property in its best light.”

A real estate professional can help you with expertise in getting your house ready to sell.

Bottom Line

If you’re considering selling your house, let’s connect so you have help navigating the process while prioritizing these must-do’s.

People Are Still Moving, Even with Today’s Affordability Challenges

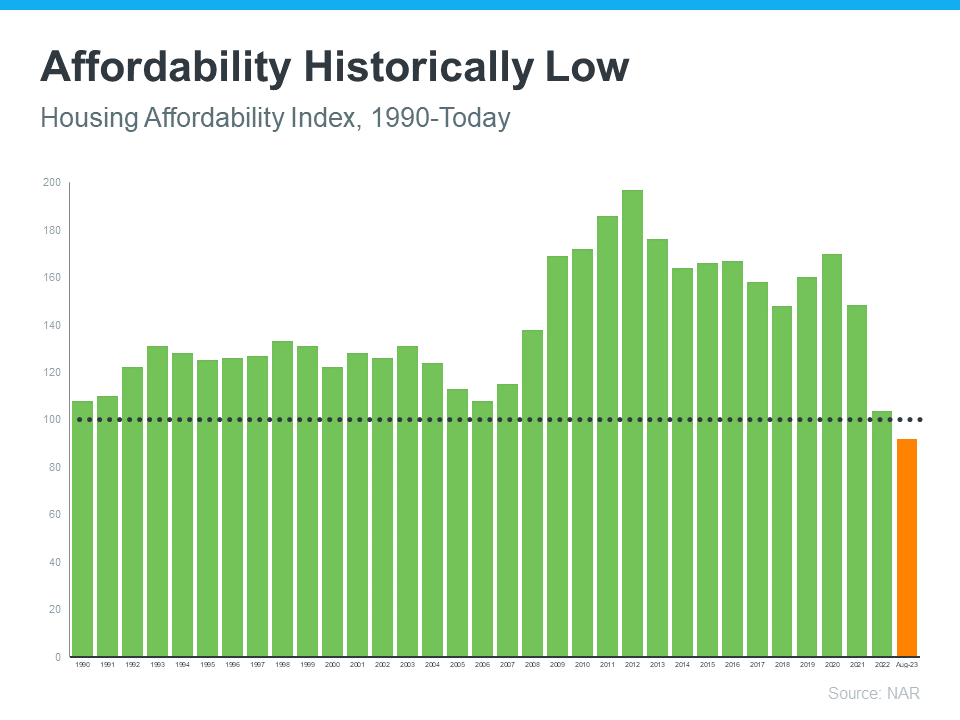

If you’re thinking about buying or selling a home, you might have heard that it’s tough right now because mortgage rates are higher than they’ve been over the past few years, and home prices are rising. That much is true. Take a look at the graph below. It breaks down how the current affordability situation stacks up to recent years.

The National Association of Realtors (NAR) explains how to read the values on the graph:

“To interpret the indices, a value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home.”

The black dotted line represents that 100 value on the index. Essentially, the higher the bar, the more affordable homes are. As you can see, the orange bar for today shows higher mortgage rates and home prices have created a clear challenge. But, while affordability is definitely tighter right now, that doesn’t mean the housing market is at a standstill.

According to NAR, based on the pace of sales right now, just under 4 million homes will sell this year. With some simple math, let’s break down what that really means for you:

- 3.96 million homes divided by 365 days in a year = 10,849 houses sell each day

- 10,849 divided by 24 hours in a day = 452 houses sell per hour

- 452 divided by 60 minutes in an hour = about 8 houses sell each minute

So, on average, over 10,000 homes sell each day in this country. Whether you’re a buyer or a seller, this goes to show there are still ways to make your move possible, even at a time when affordability is tight.

An Agent Can Help You Make Your Move a Reality

You may be wondering how other homebuyers and sellers are making this happen now. One of the biggest game-changers in today’s market is working with a trusted local real estate agent. Great agents are helping other people just like you navigate today’s market and the current affordability situation, and their insight is invaluable right now.

True professionals will be able to offer advice tailored to your specific wants, needs, budget, and more. Not to mention, they’ll also be able to draw on their experience of what’s working for other buyers and sellers right now. This could mean broadening your search, if needed, to include other housing types like condos, townhouses, or neighborhoods a bit further out to help offset some of the affordability challenges today.

Bottom Line

You might think there aren’t many people buying or selling homes right now since affordability is tighter than it’s been in quite some time, but that’s not the case. It’s true that buying a home has become more expensive over the past couple of years, but people are still moving.

If you’re hoping to buy or sell a home today, know that other people are still making their goals a reality – and that’s happening in large part because of the help and advice of skilled local real estate agents. Want to talk to a trusted professional about your own move? Let’s connect.

A Real Estate Agent Helps Take the Fear Out of the Market

Do negative headlines and talk on social media have you feeling worried about the housing market? Maybe you’ve even seen or heard something lately that scares you and makes you wonder if you should still buy or sell a home right now.

Regrettably, when news in the media isn’t easy to understand, it can make people feel scared and unsure. Similarly, negative talk on social media spreads fast and creates fear. As Jason Lewris, Co-Founder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

But it doesn’t have to be that way. Buying a home is a big decision, and it should be one you feel confident making. You should lean on a trusted real estate agent to help you separate fact from fiction and get the answers you need.

That agent will use their knowledge of what’s really happening with home prices, housing supply, expert forecasts, and more to give you the best possible advice. The National Association of Realtors (NAR) explains:

“. . . agents combat uncertainty and fear with a combination of historical perspective, training and facts.”

The right agent will help you figure out what’s going on at the national level and in your local area.

They’ll debunk headlines using data you can trust. Plus, they have in-depth knowledge of the industry and can provide context, so you know how current trends compare to the normal ebbs and flows in the housing market, historical data, and more.

Then, to make sure you have the full picture, an agent can tell you if your local area is following the national trend or if they’re seeing something different in your market. Together, you can use all that information to make the best possible decision.

After all, making a move is a potentially life-changing milestone. It should be something you feel ready for and excited about. And that’s where a trusted expert comes in.

Bottom Line

If you need reliable information about the housing market and expert advice about your own move, let’s connect.

Why You May Still Want To Sell Your House After All

Even though you may feel reluctant to sell your house because you don’t want to take on a mortgage rate that’s higher than the one you have now, there’s more to consider. While the financial side of things does matter, your personal needs may actually matter just as much. As an article from Bankrate says:

“Deciding whether it’s the right time to sell your home is a very personal decision. There are numerous important questions to consider, both financial and lifestyle-based, before putting your home on the market.”

So, ask yourself this: Why did I want to move in the first place?

Chances are your primary motivation wasn’t just financial in nature. Why you’re really thinking about selling likely has more to do with something changing in your life or a shift in what you need out of your house.

Reasons Homeowners Still Need To Sell Today

Let’s explore some of the most common reasons sellers are moving today. A recent article from Builder Online helps shed light on this. In this research, they identified the following categories:

- Marriage – If you just got married, you may find you either need more space than you currently have, or the two of you want to find a new place you picked out together.

- Divorce – If you’re getting separated or are divorcing your partner, chances are it’ll be difficult to live under the same roof. Selling the place you have, so you can own get your own spot, may be necessary.

- Births – If your household is growing, you may need more square footage, including more bedrooms. If you’re running out of room for everyone, you may not be able to wait to move.

- Deaths – If you’ve recently lost a loved one, it can be hard to spend time in that home. You may need to move for financial reasons or because you no longer need all the space.

- Retirement – If you’re in the process of retiring, or you just did, you may be looking to downsize to cut costs, relocate to be closer to loved ones, or move to a dream location. In this new phase of life, your current home may not be able to deliver what you need.

You may find you share one of these top motivators. If any of these resonate with you, it may be time to move so you can find a house better suited to your changing needs. A survey from Realtor.com finds other sellers are in the same boat. It says, 1 in 4 sellers are choosing to move for personal reasons, even with current mortgage rates:

“. . . more than half of seller-buyers (56%) who are planning to sell in the next 12 months said they are waiting for rates to come down, while 25% need to sell soon for personal reasons.”

If you need to sell now because something in your own life has changed, don’t let rates hold you back from what you want. You have options to help make that move possible. You can use the equity you already have in your current home toward your next purchase. And with how much equity homeowners have right now, you may be able to finance less than you’d expect or pay all cash to avoid borrowing at all.

Bottom Line

When you’re ready to prioritize your changing needs, let’s connect. You need an expert on your side to help you list your house and find a home that delivers everything you’re looking for.

Don’t Fall for the Next Shocking Headlines About Home Prices

If you’re thinking of buying or selling a home, one of the biggest questions you have right now is probably: what’s happening with home prices? And it’s no surprise you don’t have the clarity you need on that topic. Part of the issue is how headlines are talking about prices.

They’re basing their negative news by comparing current stats to the last few years. But you can’t compare this year to the ‘unicorn’ years (when home prices reached record highs that were unsustainable). And as prices begin to normalize now, they’re talking about it like it’s a bad thing and making people fear what’s next. What we’re starting to see now is the return to more normal home price appreciation.

To help make home price trends easier to understand, let’s focus on what’s typical for the market and omit the last few years since they were anomalies.

Let’s start by talking about seasonality in real estate. In the housing market, there are predictable ebbs and flows that happen each year. Spring is the peak homebuying season when the market is most active. That activity is typically still intense in the summer but begins to wane as the cooler months approach. Home prices follow along with seasonality because prices appreciate most when something is in high demand.

That’s why, before the abnormal years we just experienced, there was a reliable long-term home price trend. The graph below uses data from Case-Shiller to show typical monthly home price movement from 1973 through 2021 (not adjusted, so you can see the seasonality):

As the data from the last 48 years shows, at the beginning of the year, home prices grow, but not as much as they do entering the spring and summer markets. That’s because the market is less active in January and February since fewer people move in the cooler months. As the market transitions into the peak homebuying season in the spring, activity ramps up, and home prices go up a lot more in response. Then, as fall and winter approach, activity eases again. Price growth slows, but still typically appreciates.

Why This Is So Important to Understand

In the coming months, as the housing market moves further into a more predictable seasonal rhythm, you’re going to see even more headlines that either get what’s happening with home prices wrong or, at the very least, are misleading. Those headlines might use a number of price terms, like:

- Appreciation: when prices increase.

- Deceleration of appreciation: when prices continue to appreciate, but at a slower or more moderate pace.

- Depreciation: when prices decrease.

They’re going to mistake the slowing home price growth (deceleration of appreciation) that’s typical of market seasonality in the fall and winter and think prices are falling (depreciation). Don’t let those headlines confuse you or spark fear. Instead, remember it’s normal to see a deceleration of appreciation, slowing home price growth, as the months go by.

Bottom Line

If you have questions about what’s happening with home prices in our local area, let’s connect.

Why Buying or Selling a Home Helps the Economy and Your Community

If you’re thinking about buying or selling a house, it’s important to know that it doesn’t just affect your life, but also your community.

The National Association of Realtors (NAR) releases a report every year to show how much economic activity is generated by home sales. The chart below illustrates that impact:

As the visual shows, when a house is sold, it can make a big difference in the local economy. The impact comes largely from the workers required to build, update, and buy and sell homes. Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), explains how the housing industry adds jobs to a community:

“The economic impact means housing is a significant job creator. In fact, for every single-family home built, enough economic activity is generated to sustain three full-time jobs for a year, per NAHB research. . . . And one job for every $100,000 in remodeling spending.”

Housing being a major job creator makes sense when you consider there are many different industries involved in the process. A recent article from Fortune notes housing activity could have a more robust impact than you think due to the many ways it’s tied to the economy:

“Housing has three direct linkages to economic activity (GDP): the construction of new homes, the remodeling of existing homes, and that of housing transactions. . . . consider the activity associated with home sales – think broker fees, lawyers, etc. – which are a sizable contributor to housing’s GDP footprint.”

When you buy or sell a home, you work with a team of professionals, including contractors, specialists, lawyers, and city officials. Each person plays a role in making the transaction happen.

So, when you make a move in the housing market, you’re not just meeting your own needs, you’re also making a positive impact on the community. Knowing this can give you a sense of empowerment as you make your decision this year.

Bottom Line

Each and every home sale is important for the local economy. If you’re ready to move, let’s connect. It won’t just change your life – it’ll also have a strong positive effect on the whole community.

The Three Factors Affecting Home Affordability Today

There’s been a lot of focus on higher mortgage rates and how they’re creating affordability challenges for today’s homebuyers. It’s true that rates have climbed since the record-low we saw during the pandemic. But home affordability is based on more than just mortgage rates – it’s determined by a combination of mortgage rates, home prices, and wages.

Considering how each one of these factors is changing gives you the full picture of home affordability today. Here’s the latest.

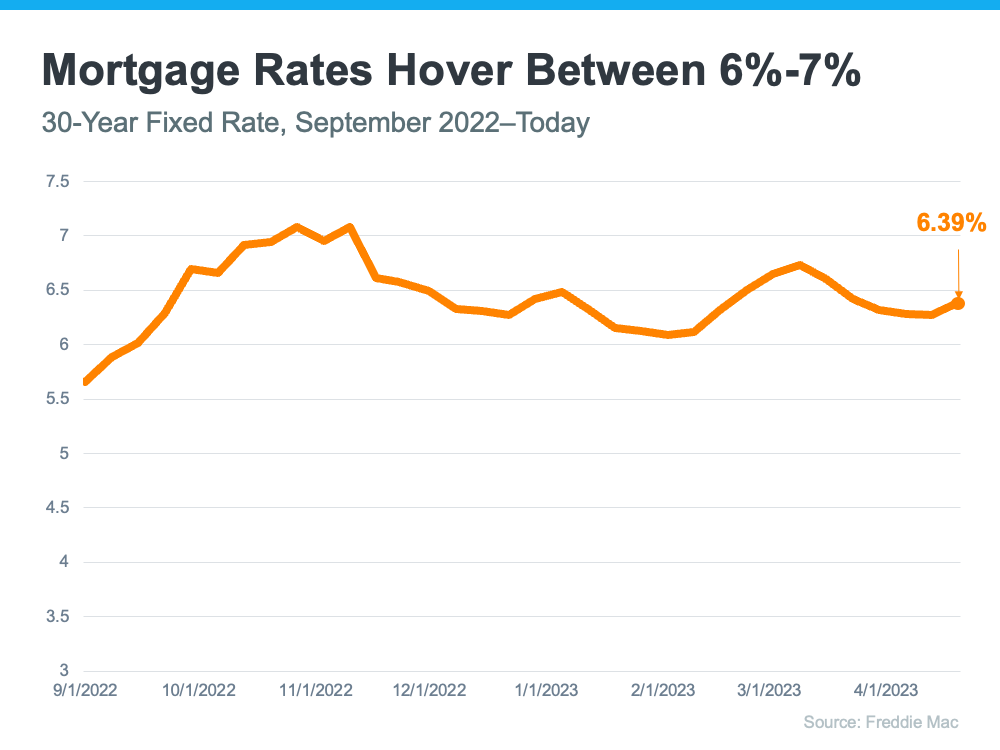

1. Mortgage Rates

While mortgage rates are higher than they were a year ago, they’ve hovered primarily between 6% and 7% for nearly eight months now (see graph below):

As the graph shows, mortgage rates have experienced some volatility during that time. And even a small change in mortgage rates impacts your purchasing power. That’s why it’s so important to lean on your team of real estate professionals for expert advice to stay up to date on what’s happening in the market. While it’s hard to project where mortgage rates will go from here, many experts agree they’ll likely continue to remain around 6%-7% in the immediate future.

2. Home Prices

Over the past few years, home prices appreciated rapidly as the record-low mortgage rates we saw during the pandemic led to a surge in buyer demand. The heightened buyer demand happened while the supply of homes for sale was at record lows, and that imbalance put upward pressure on home prices. However, today’s higher mortgage rates have slowed down price appreciation.

And, the truth is, home price appreciation varies by market. Some areas are seeing slight declines while others have prices that are climbing. As Selma Hepp, Chief Economist at CoreLogic, explains:

“The divergence in home price changes across the U.S. reflects a tale of two housing markets. Declines in the West are due to the tech industry slowdown and a severe lack of affordability after decades of undersupply. The consistent gains in the Southeast and South reflect strong job markets, in-migration patterns and relative affordability due to new home construction.”

To find out what’s happening with prices in your local market, reach out to a trusted real estate agent.

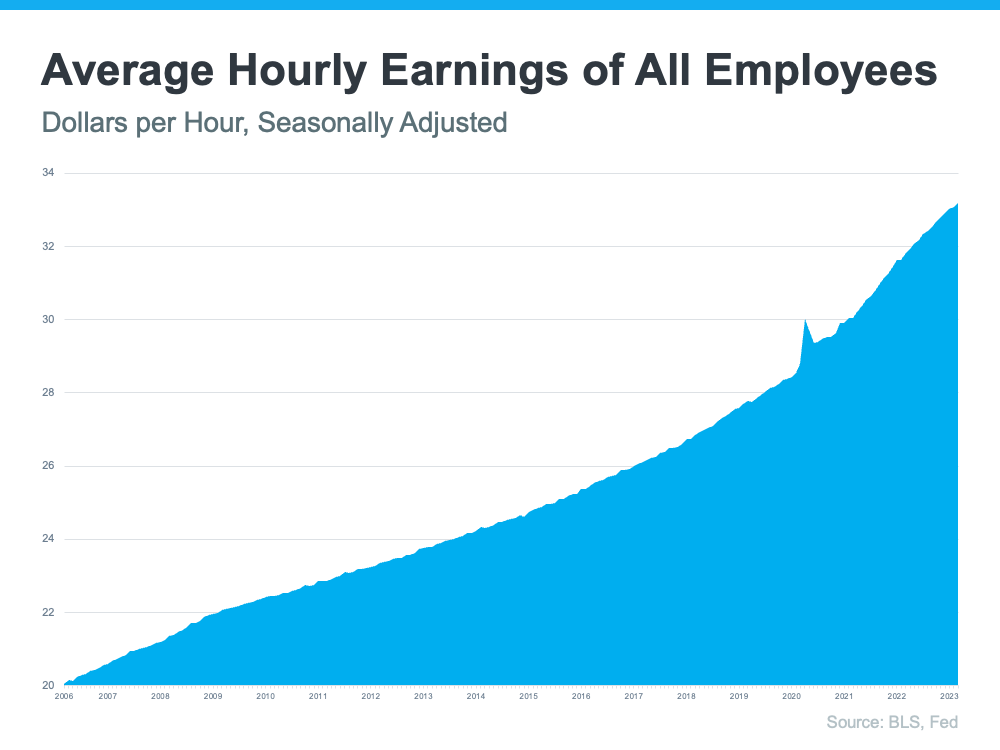

3. Wages

The most positive factor in affordability right now is rising income. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have grown over time:

Higher wages improve affordability because they reduce the percentage of your income it takes to pay your mortgage since you don’t have to put as much of your paycheck toward your monthly housing cost.

Home affordability comes down to a combination of rates, prices, and wages. If you have questions or want to learn more, reach out to a real estate professional who can explain what’s happening locally and how these factors work together.

If you’re planning to buy a home, knowing the key factors that impact affordability is important so you can make an informed decision. To stay up to date on the latest on each, let’s connect today.

Bottom Line

Why Buying a Home Is a Sound Decision

If you’re thinking about buying a home, you want to know if the decision will be a good one. And for many, that means thinking about what home prices are projected to do in the coming years and how that could impact your investment.

This year, we aren’t seeing home prices fall dramatically. As the year goes on, however, some markets may go up in value while others may lose value. That’s why it’s helpful to keep the long-term view in mind. Experts project a return to a steadier rate of price appreciation in the years that follow.

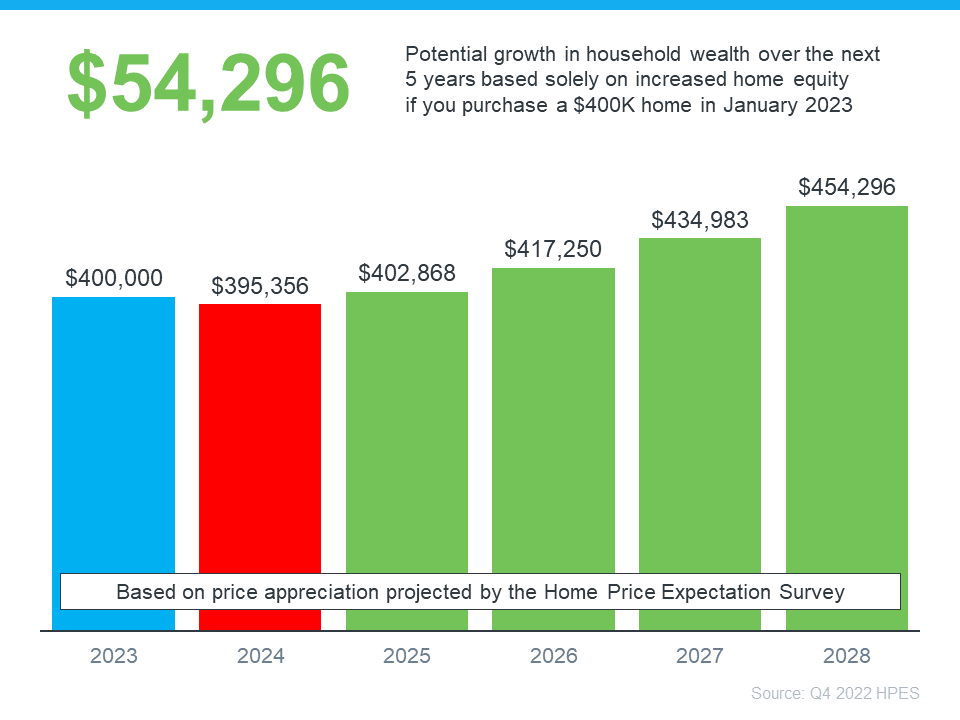

Home Price Appreciation in the Years Ahead

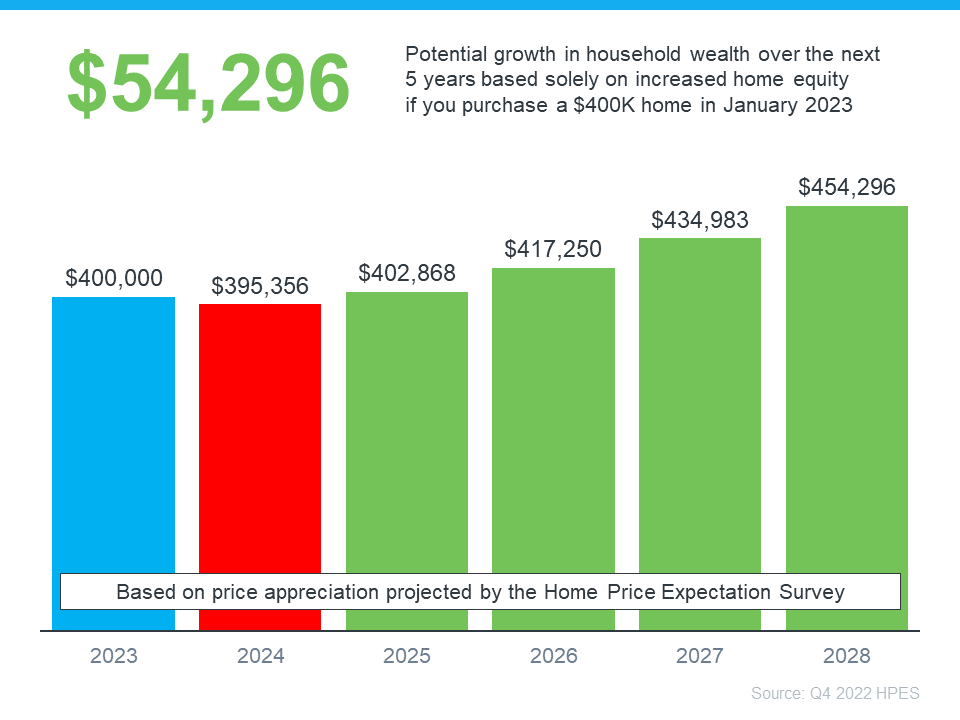

Over 100 economists, investment strategists, and housing market analysts were polled by Pulsenomics in their latest quarterly Home Price Expectation Survey (HPES). The report indicates what they believe will happen with home prices over the next five years. As the graph below shows, after mild depreciation this year, these experts forecast home prices will return to more normal levels of appreciation through 2027.

The big takeaway is experts aren’t forecasting a drastic fall in home prices nationally, even though some markets will see home price appreciation while others may depreciate. And when they look further out, they see steady price appreciation in the long run. That’s a great example of why homeownership wins over time.

What Does This Mean for You?

Once you buy a home, price appreciation raises your home’s value, and that grows your household wealth. Here’s how a typical home’s value could change over the next few years using the expert price appreciation projections from the survey mentioned above (see graph below):

Once you buy a home, price appreciation raises your home’s value, and that grows your household wealth. Here’s how a typical home’s value could change over the next few years using the expert price appreciation projections from the survey mentioned above (see graph below):

In this example, if you bought a $400,000 home at the beginning of this year and factor in the forecast from the HPES, you could accumulate over $54,000 in household wealth over the next five years. So, if you’re wondering if buying a home is a sound decision, keep in mind what a strong wealth-building tool it is long term.

Bottom Line

According to the experts, while we may see slight depreciation this year, home prices are expected to grow over the next five years. If you’re ready to become a homeowner, know that buying today can set you up for long-term success as home values (and your own net worth) are projected to grow.

Let’s connect to begin the homebuying process today.

Spring into Action: Boost Your Home’s Curb Appeal with Expert Guidance

To sell your home this spring, it may need more preparation than it would have a year or two ago. Today’s housing market has a different feel. There are more homes for sale than at this time last year, but inventory is still historically low. So, if a house has been sitting on the market for a while, that’s a sign it may not be hitting the mark for potential buyers. But here’s the thing. Right now, homes that are updated and priced at market value are still selling fast.

Today, homes with curb appeal that are presented well are still selling quickly, and sometimes over the asking price. According to Danielle Hale, Chief Economist at realtor.com:

“In a market where costs are still high and buyers can be a little choosier, it makes sense they’re going to really zero in on the homes that are the most appealing.”

With the spring buying season just around the corner, now’s the time to start getting your house ready to sell. And the best way to determine where to spend your time and money is to work with a trusted real estate agent who can help you understand which improvements are most valuable in your local market.

Curb Appeal Wins

One way to prioritize updates that could bring a good return on your investment is to find smaller projects you can do yourself. Little updates that boost your curb appeal usually work well. Investopedia puts it this way:

“Curb-appeal projects make the property look good as soon as prospective buyers arrive. While these projects may not add a considerable amount of monetary value, they will help your home sell faster—and you can do a lot of the work yourself to save money and time.”

Small cosmetic updates, like refreshing some paint and power washing the exterior of your home, create a great first impression for buyers and help it stand out. Work with a real estate professional to find low-cost projects you can tackle around your house that will appeal to buyers in your area.

Not All Updates Are Created Equal

When deciding what you need to do to your house before selling it, remember you’re making these repairs and updates for someone else. Prioritize projects that will help you sell faster or for more money over things that appeal to you as a homeowner.

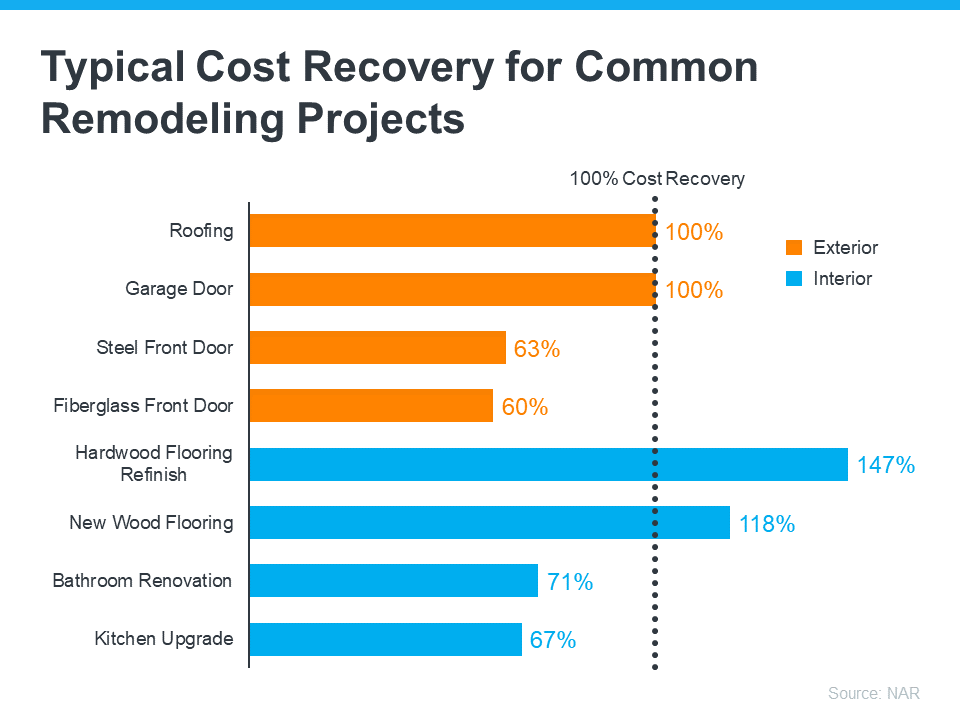

The 2022 Remodeling Impact Report from the National Association of Realtors (NAR) highlights popular home improvements and what sort of return they bring for the investment (see graph below):

Remember to lean on your trusted real estate advisor for the best advice on the updates you should invest in. They’ll know what local buyers are looking for and have the latest insights into what your house needs to sell quickly this spring.

Bottom Line

As we approach the spring season, now’s the time to get your house ready to sell.

Let’s connect today to find out which updates make the most sense.

3 Ways You Can Use Your Home Equity

If you’re a homeowner, odds are your equity has grown significantly over the last few years as home prices skyrocketed and you made your monthly mortgage payments. Home equity builds over time and can help you achieve certain goals. According to the latest Equity Insights Report from CoreLogic, the average borrower with a home loan has almost $300,000 in equity right now.

As you weigh your options, especially in the face of inflation and talk of a recession, it’s important to understand your assets and how you can leverage them. A real estate professional is the best resource to help you understand how much home equity you have and advise you on some of the ways you can use it. Here are a few examples.

1. Buy a Home That Fits Your Needs

If you no longer have the space you need, it might be time to move into a larger home. Or it’s possible you have too much space and need something smaller. No matter the situation, consider using your equity to power a move into a home that fits your changing lifestyle.

If you want to upgrade your house, you can put your equity toward a down payment on the home of your dreams. And if you’re planning to downsize, you may be surprised that your equity may cover some, if not all, of the cost of your next home. A real estate advisor can help you figure out how much equity you have and how you can use it toward the purchase of your next home.

2. Reinvest in Your Current House

According to a recent survey from Point, 39% of homeowners would invest in home improvement projects if they chose to access their equity. This is a great option if you want to change some things about your living space but you aren’t ready to make a move just yet.

Home improvement projects allow you to customize your home to suit your needs and sense of style. Just remember to think ahead with any updates you make, as some renovations add more value to your home and are more likely to appeal to future buyers than others. For example, a report from the National Association of Realtors (NAR) shows refinishing or replacing wood flooring has a high cost recovery. Lean on a local professional for the best advice on which projects to invest in to get the greatest return on your investment when you sell.

3. Pursue Your Personal Goals

In addition to making a move or updating your house, home equity can also help you achieve the life goals you’ve dreamed of. That could mean investing in a new business venture, retiring or downsizing, or funding an education. While you shouldn’t use your equity for unnecessary spending, leveraging it to start a business or putting it toward education costs can help you achieve other lifelong goals.

Bottom Line

Your equity can be a game changer. If you’re unsure how much equity you have in your home, let’s connect so you can start planning your next move.

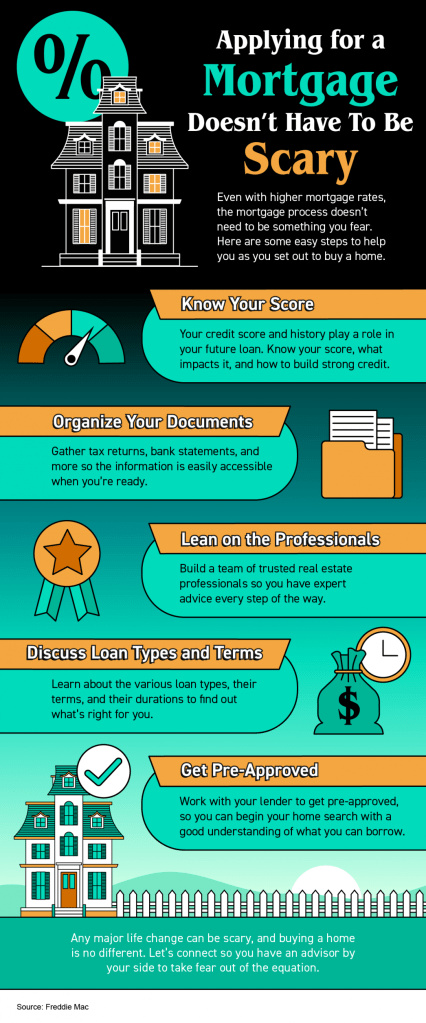

Taking the Fear out of Saving for a Home

If you’re planning to buy a home, knowing what to budget for and how to save may sound scary at first. But it doesn’t have to be. One way to take the fear out of budgeting is to understand some of the costs you might encounter. And to do that, turn to trusted real estate professionals. They can help you plan your finances and prepare your budget.

Here are just a few costs experts say you can expect.

1. Down Payment

Saving for your down payment is likely at top of your mind as you set out to buy a home. But do you know how much you’ll need to save? While each situation is different, there’s a common misconception that putting 20% down toward your purchase is required. An article from the Mortgage Reports explains why that’s not always the case:

“The idea that you have to put 20% down on a house is a myth. . . . The right amount depends on your current savings and your home buying goals.”

To understand your options, partner with a trusted real estate professional to go over the various loan types, down payment assistance programs, and what each one requires.

2. Closing Costs

Make sure you also budget for closing costs, which are a collection of fees and payments made to the various people involved in your transaction. Bankrate explains:

“Closing costs are the fees you pay when finalizing a real estate transaction, whether you’re refinancing a mortgage or buying a new home. These costs can amount to 2 to 5 percent of the mortgage so it’s important to be financially prepared for this expense.”

The best way to understand what you’ll need at the closing table is to work with a trusted lender. They can provide you with answers to the questions you might have.

3. Earnest Money Deposit

If you want to cover all your bases, you can also consider saving for an earnest money deposit (EMD). An EMD is a money you pay as a show of good faith when you make an offer on a house. According to realtor.com, it’s usually between 1% and 2% of the total home price.

This deposit works like a credit. It’s not an added expense – it’s paying a portion of your costs upfront. You’re using some of the money you already saved for your purchase to show the seller you’re committed and serious about their house. Realtor.com describes how it works as part of your sale:

“It tells the real estate seller you’re in earnest as a buyer, . . . . Assuming that all goes well and the buyer’s good-faith offer is accepted by the seller, the earnest money funds go toward the down payment and closing costs. In effect, earnest money is just paying more of the down payment and closing costs upfront.”

Keep in mind, an EMD isn’t required, and it doesn’t guarantee your offer will be accepted. It’s important to work with a real estate advisor to understand what’s best for your situation and any specific requirements in your area. They’ll help you determine what moves you should make in the home-buying process to have the greatest success.

Bottom Line

Budgeting for your home purchase doesn’t have to be scary. Let’s connect so you’ll have an expert on your side to answer any questions you have along the way.

Top Reasons Homeowners Are Selling Their Houses Right Now

Some people believe there’s a group of homeowners who may be reluctant to sell their houses because they don’t want to lose the historically low mortgage rate they have on their current homes. You may even have the same hesitation if you’re thinking about selling your house.

Data shows that 51% of homeowners have a mortgage rate under 4% as of April this year. And while it’s true mortgage rates are higher than that right now, there are other non-financial factors to consider when it comes to making a move. In other words, your mortgage rate is important, but you may have other things going on in your life that make a move essential, regardless of where rates are today. As Jessica Lautz, Vice President of Demographics and Behavioral Insights at the National Association of Realtors (NAR), explains:

“Home sellers have historically moved when something in their lives changed – a new baby, a marriage, a divorce or a new job. . . .”

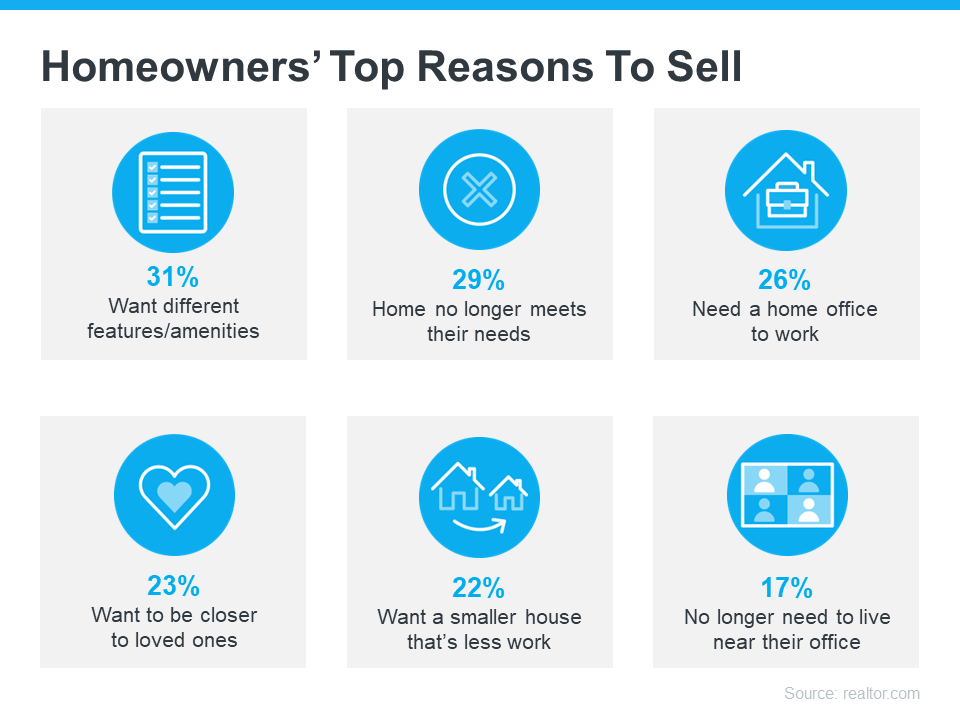

So, if you’re thinking about selling your house, it may help to explore the other reasons homeowners are choosing to make a move today. The 2022 Summer Sellers Survey by realtor.com asked recent home sellers why they decided to sell. The visual below breaks down how those homeowners responded:

As the visual shows, an appetite for different features or the fact that their current home could no longer meet their needs topped the list for recent sellers. Additionally, remote work and whether or not they need a home office or are tied to a specific physical office location also factored in, as did the desire to live close to their loved ones.

The realtor.com survey summarizes the findings like this:

“The primary reason homeowners decided to sell in the last year was the realization that, after so much time spent at home, they wanted different features and amenities, such as walkability, outdoor space, pool, etc. . . . ”

If you, like the homeowners they surveyed, find yourself wanting features, space, or amenities your current home just can’t provide, it may be time to consider listing your house for sale.

Even with today’s mortgage rates, your lifestyle needs may be enough to motivate you to make a change. The best way to find out what’s right for you is to partner with a trusted real estate professional who can provide expert guidance and advice throughout the process. They can help walk you through your options, so you can make a confident decision based on what matters most to you and your loved ones.

Bottom Line

While the financial reasons for moving are important, there’s often far more to consider. Non-financial reasons can also be a significant motivating factor. If you need help weighing the pros and cons of selling your house, let’s connect today.

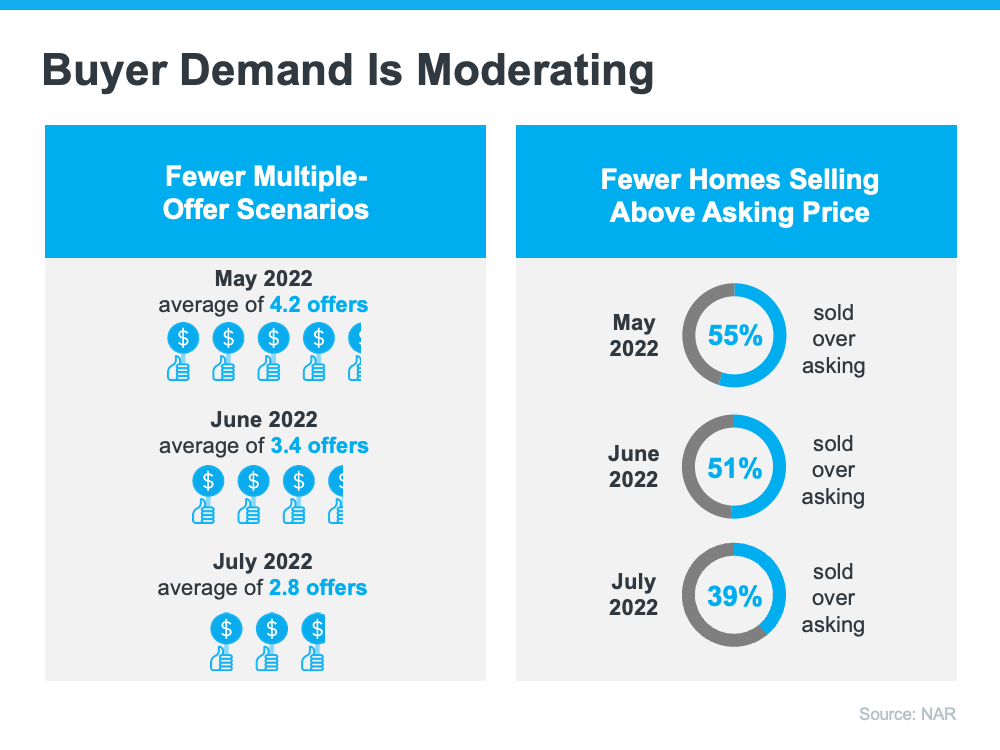

What Sellers Need To Know in Today’s Housing Market

If you’re thinking about selling your house, you may have heard about the housing market slowing down in recent months. While it’s still a sellers’ market, the peak frenzy the market saw over the past two years has cooled some. If you’re asking yourself if you’ve missed your chance to sell your house and make a move, the good news is you haven’t – motivated buyers are still out there. But you do need to price your house right for today’s market. Here’s why.

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Homes priced right are selling very quickly, but homes priced too high are deterring prospective buyers.”

It’s true buyer demand has slowed over the past few months as higher mortgage rates made it more expensive to buy a home. The result is fewer bidding wars and less competition among buyers (see visual below):

But don’t forget – that’s compared to the severely overheated market we saw over the past two years. According to the latest Confidence Index from NAR:

“. . . 39% of homes sold above list price, down from 51% a month ago and 50% a year ago.”

While this is a slower pace than even one month ago, serious buyers are still in the market, and they’re buying homes that are priced right. In fact, the Confidence Index also notes the average home is selling in just 14 days.

If you’re aiming to sell your house, be sure you’re working with your agent to price it for today’s housing market. As buyer demand softens, it’s important to understand this isn’t the same market as last year. It’s not even the same market as just a few months ago. But it is still a sellers’ market.

If you’re ready to sell your house, seek the advice of a real estate professional. In some cases, you’ll need to adjust your expectations accordingly to meet the market where it is today. Selma Hepp, Interim Lead, Deputy Chief Economist at CoreLogic, explains what’s happening and what it means when you sell:

“Signs of a broader slowdown in the housing market are evident, . . . This is in line with our previous expectations and given the notable cooling of buyer demand due to higher mortgage rates. . . . Nevertheless, buyers still remain interested, which is keeping the market competitive — particularly for attractive homes that are properly priced.”

Bottom Line

While the housing market has cooled from its overheated frenzy, it’s still a sellers’ market. Let’s connect so you understand what’s happening with buyer demand and home prices in our local area as you get ready to enter the market.

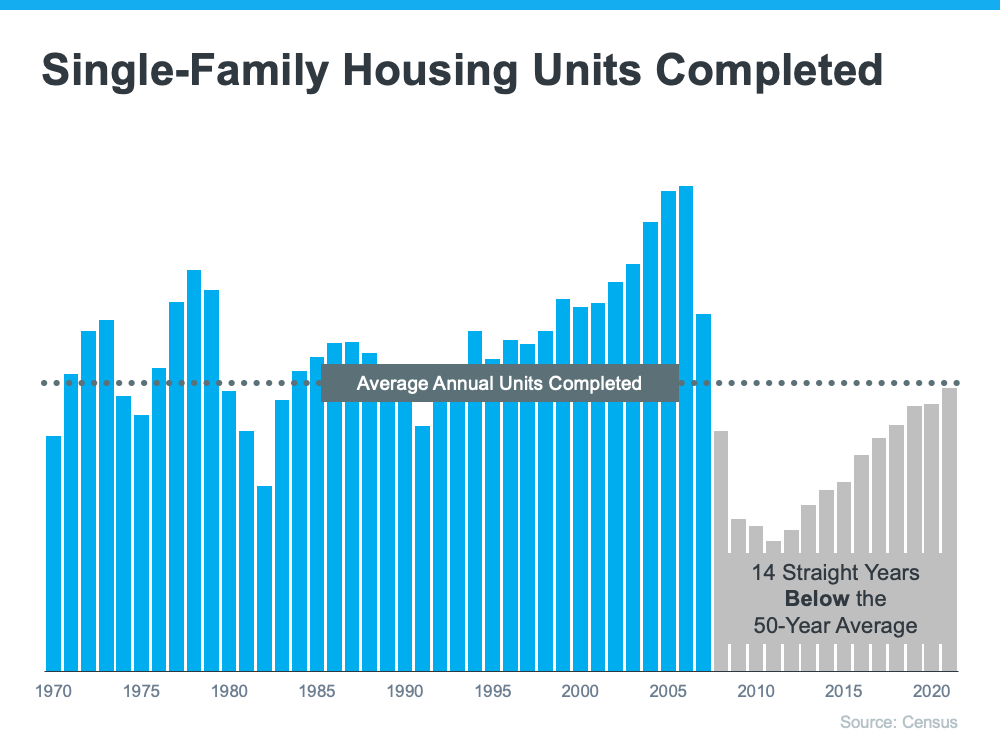

What’s Causing Ongoing Home Price Appreciation?

If you’re thinking about making a move, you probably want to know what’s going to happen to home prices for the rest of the year. While experts say price growth will moderate due to the shifting market, ongoing appreciation is expected. That means home prices won’t fall. Here’s a look at two key reasons experts forecast continued price growth: supply and demand.

While Growing, Housing Supply Is Still Low

Even though inventory is increasing this year as the market moderates, supply is still low. The graph below helps tell the story of why there still aren’t enough homes on the market today. It uses data from the Census to show the number of single-family homes that were built in this country going all the way back to the 1970s.

The blue bars represent the years leading up to the housing crisis in 2008. As the graph shows, right before the crash, homebuilding increased significantly. That’s because buyer demand was so high due to loose lending standards that enabled more people to qualify for a home loan.

The resulting oversupply of homes for sale led to prices dropping during the crash and some builders leaving the industry or closing their businesses – and that led to a long period of underbuilding of new homes. And even as more new homes are constructed this year and in the years ahead, this isn’t something that can be resolved overnight. It’ll take time to build enough homes to meet the deficit of underbuilding that took place over the past 14 years.

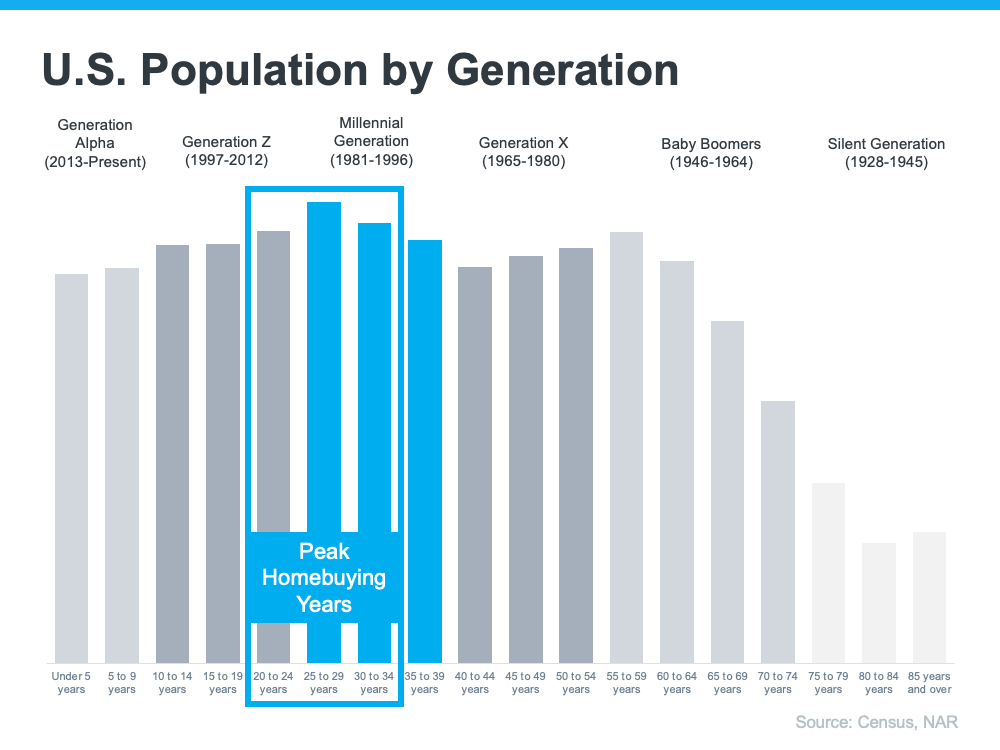

Millennials Will Create Sustained Buyer Demand Moving Forward

The frenzy the market saw during the pandemic is because there was more demand than homes for sale. That drove home prices up as buyers competed with one another for available homes. And while buyer demand has moderated today in response to higher mortgage rates, data tells us demand will continue to be driven by the large generation of millennials aging into their peak homebuying years (see graph below):

Odeta Kushi, Deputy Chief Economist at First American, explains:

“. . . millennials continue to transition to their prime home-buying age and will remain the driving force in potential homeownership demand in the years ahead.”

That combination of millennial demand and low housing supply continues to put upward pressure on home prices. As Bankrate says:

“After all, supplies of homes for sale remain near record lows. And while a jump in mortgage rates has dampened demand somewhat, demand still outpaces supply, thanks to a combination of little new construction and strong household formation by large numbers of millennials.”

What This Means for Home Prices

If you’re worried home values will fall, rest assured that experts forecast ongoing home price appreciation thanks to the lingering imbalance of supply and demand. That means home prices won’t decline.

Bottom Line

Based on today’s factors driving supply and demand, experts project home price appreciation will continue. It’ll just happen at a more moderate pace as the housing market continues its shift back toward pre-pandemic levels.

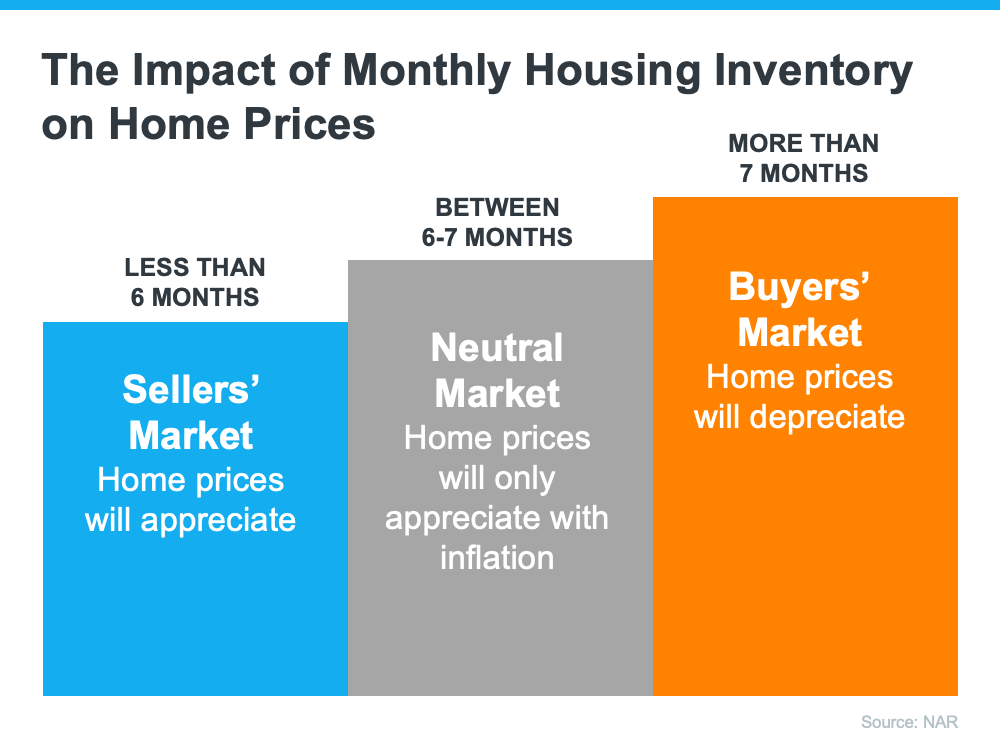

What You Need To Know About Selling in a Sellers’ Market

Even if you haven’t been following real estate news, you’ve likely heard about the current sellers’ market. That’s because there’s a lot of talk about how strong market conditions are for people who want to sell their houses. But if you’re thinking about listing your house, you probably want to know: what does being in a sellers’ market really mean?

What Is a Sellers’ Market?

The latest Existing Home Sales Report from the National Association of Realtors (NAR) shows housing supply is still very low. There’s a 2-month supply of homes at the current sales pace.

Historically, a 6-month supply is necessary for a normal or neutral market where there are enough homes available for active buyers. That puts today deep in sellers’ market territory (see graph below):

What Does This Mean for You When You Sell?

When the supply of houses for sale is as low as it is right now, it’s much harder for buyers to find homes to purchase. That creates increased competition among purchasers which can lead to more bidding wars. And if buyers know they may be entering a bidding war, they’re going to do their best to submit a very attractive offer upfront. This could drive the final price of your house up.

And because mortgage rates and home prices are climbing, serious buyers are motivated to make their purchase soon, before those two things rise further. That means, if you put your house on the market while supply is still low, it will likely get a lot of attention from competitive buyers. Setting you up to be in a great position to cash in on all that added equity your home has been gaining!

Bottom Line

The current real estate market has incredible opportunities for homeowners looking to make a move. Listing your house this season means you’ll be in front of serious buyers who are ready to buy. Let’s connect so you can jumpstart the selling process.

What You Can Expect from the Spring Housing Market

As the spring housing market kicks off, you likely want to know what you can expect this season when it comes to buying or selling a house. While there are multiple factors causing some uncertainty, including the conflict overseas, rising inflation, and the first-rate increase from the Federal Reserve in over three years — the housing market seems to be relatively immune.

Here’s a look at what experts say you can expect this spring.

1. Mortgage Rates Will Climb

Freddie Mac reports the 30-year fixed mortgage rate has increased by more than a full point in the past six months. And despite some mild fluctuation in recent weeks, experts believe rates will continue to edge up over the next 90 days. As Freddie Mac says:

“The Federal Reserve raising short-term rates and signaling further increases means mortgage rates should continue to rise over the course of the year.”

If you’re a first-time buyer or a seller thinking of moving to a home that better fits your needs, realize that waiting will likely mean you’ll pay a higher mortgage rate on your purchase. And that higher rate drives up your monthly payment and can really add up over the life of your loan.

2. Housing Inventory Will Increase

There may be some relief coming for buyers searching for a home to purchase. Realtor.com recently reported that the number of newly listed homes has grown in each of the last two months. Also, the National Association of Realtors (NAR) just announced the months’ supply of inventory increased for the first time in eight months. The inventory of existing homes usually grows every spring, and it seems, based on recent activity, the next 90 days could bring more listings to the market.

If you’re a buyer who has been frustrated with the limited supply of homes available for sale, it looks like you could find some relief this spring. However, be prepared to act quickly if you find the right home.

If you’re a seller, listing now instead of waiting for this additional competition to hit the market makes sense. Your leverage in any negotiation during the sale will be impacted as additional homes come to market.

3. Home Prices Will Rise

Prices are always determined by supply and demand. Though the number of homes entering the market is increasing, buyer demand remains very strong. As realtor.com explains in their most recent Housing Report:

“During the final two weeks of the month, more new sellers entered the market than during the same time last year. . . . However, with 5.8 million new homes missing from the market and millions of millennials at first-time buying ages, housing supply faces a long road to catching up with demand.”

What does that mean for you? With the demand for housing still outpacing supply, home prices will continue to appreciate. Many experts believe the level of appreciation will decelerate from the high double-digit levels we’ve seen over the last two years. That means prices will continue to climb, just at a more moderate pace. Most experts are predicting home prices will not depreciate.

Won’t Increasing Mortgage Rates Cause Home Prices To Fall?

While some people may believe a 1% increase in mortgage rates will impact demand so dramatically that home prices will have to fall, experts say otherwise. Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae, says:

“What I will caution against is making the inference that interest rates have a direct impact on house prices. That is not true.”

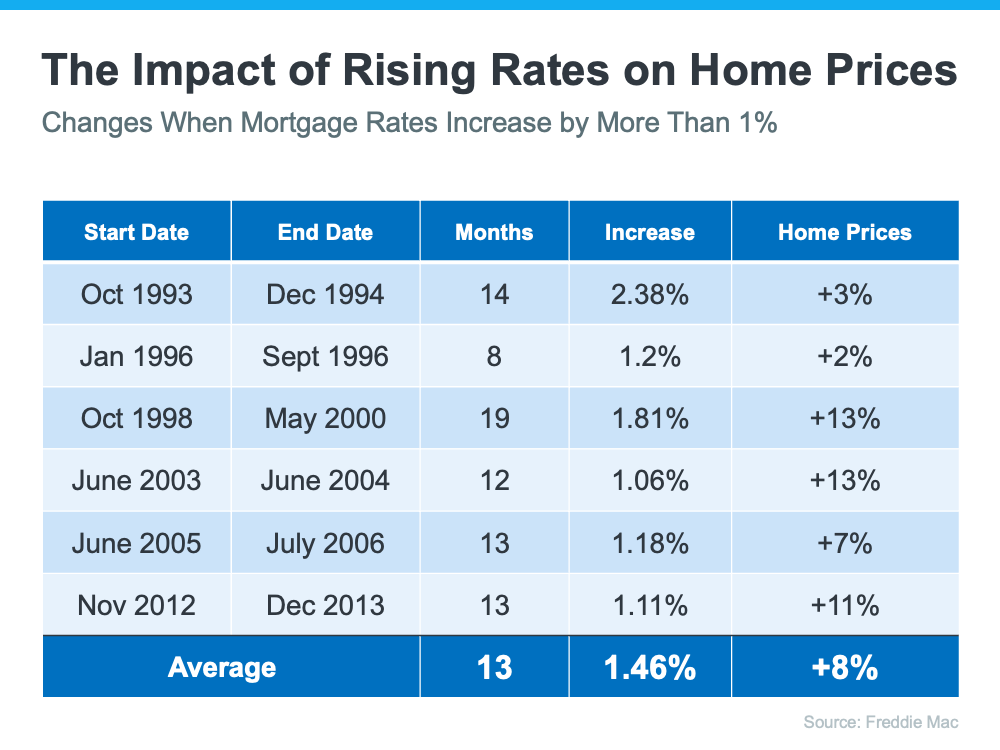

Freddie Mac studied the impact that mortgage rates increasing by at least 1% has had on home prices in the past. Here are the results of that study:

As the chart shows, mortgage rates jumped by at least 1% six times in the last thirty years. In each case, home values increased. So again, if you’re a first-time buyer or a repeat buyer, waiting to buy likely means you’ll pay more for your home later in the year (as compared to its current value).

Bottom Line

There are three things that seem certain going into the spring housing market:

- Mortgage rates will continue to rise – but it’s predicted to do so slowly and not dramatically.

- The selection of homes available for sale will modestly improve. Meaning sellers should get listed now to get the best deal possible on the sale of their home, and buyers should be ready to pounce on their dream homes quickly.

- Home prices will continue to appreciate, just at a slightly slower pace

If you’re thinking of buying, act now before mortgage rates and home prices increase further. If you’re thinking of selling, your best bet may be to sell soon so you can beat the increase in competition that’s about to come to market. Contact me today, to discuss your real estate needs & I will get to work for you!

Have questions, or want to discuss your goals, but would rather get started via email? Feel free to ask questions or let me know if you are looking to buy or sell using the contact form below & I will get in touch with you as soon as possible. If you would prefer that I give you a call, please include your phone number.

I look forward to working with you!

As Home Equity Rises, So Does Your Wealth

Homeownership is still a crucial part of the American dream. For those people who own a home (and those looking to buy one), it’s clear that being a homeowner has considerable benefits both emotionally and financially. In addition to long-term stability, buying a home is one of the best ways to increase your net worth. This boost to your wealth comes in the form of equity.

Equity is the difference between what you owe on the home and its market value based on factors like price appreciation.

The best thing about equity is that it often grows without you even realizing it, especially in a sellers’ market like we’re in now. In today’s real estate market, the combination of low housing supply and high buyer demand is driving home values up. This is giving homeowners a significant equity boost.

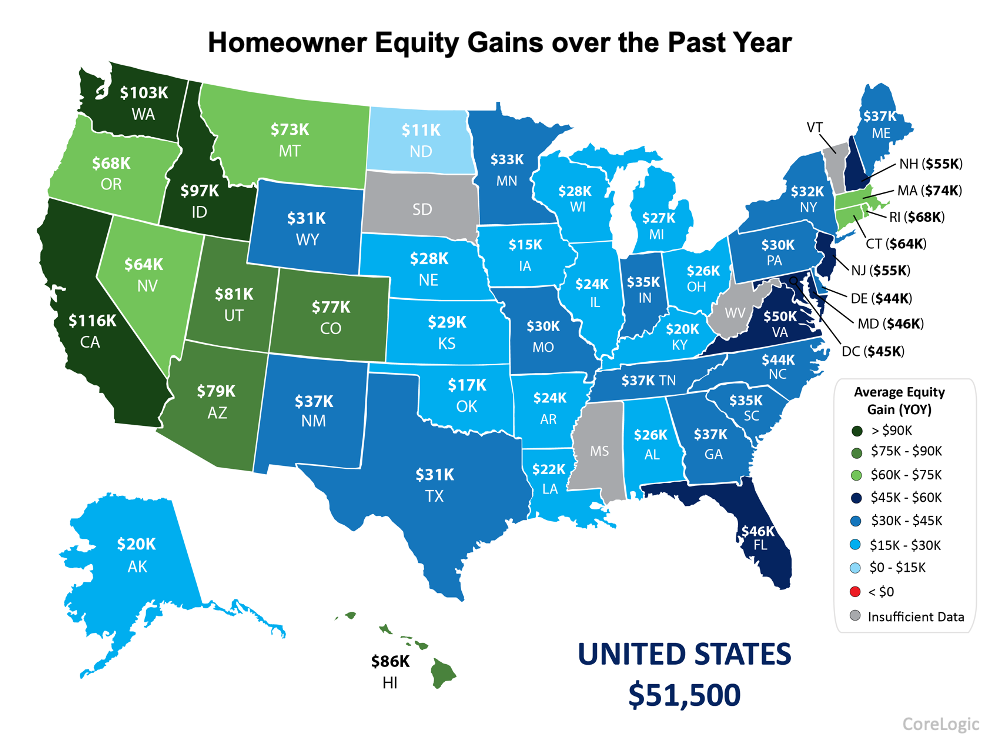

According to the latest data from CoreLogic, the amount of equity homeowners have has continued to grow as home values appreciate. Here are some key takeaways from the Homeowner Equity Insights Report:

- The average homeowner gained $51,500 in equity over the past year

- There was a 29.3% increase in national homeowner equity year over year

To give you an idea of what that looks like in your area, the map below shows the average equity gains by state.

What does all of that mean for you?

If you’re already a homeowner, you likely have more equity in your house than you realize. The numbers in the map above reflect year-over-year growth. If you’ve been in your home for longer than a year, you’ll likely have even more equity than that. That equity can take you places. You can use the equity you’ve gained to fuel your next move, achieve other life goals, and more.

On the other hand, if you haven’t purchased a home yet, understanding equity can help you realize why homeownership is a worthwhile goal. Homeowners across the nation gained an average of over $50,000 in equity this year. Don’t miss out on this chance to grow your net worth.

Bottom Line

If you want to learn more, let’s connect. I can help you understand where home prices are today, how they contribute to a homeowner’s net worth, and the impact equity can have when you own a home.

Contact me today to start the process of capitalizing on your homes equity or starting to build it by becoming a homeowner!

CALL (517) 643-1834 or EMAIL: morgan@morganrobinson.org

Stay or Sell? How To Make the Right Call as You Age

At some point, as you start thinking about the years ahead, this question tends to come up:

“Could I stay here long-term… or would it make more sense to move?”

It’s not always urgent. It often shows up in small moments, like going up and down the stairs, keeping up with the maintenance, or just thinking about what the next chapter of your life might look like in this home.

And for most people, the answer is simple. They want to stay.

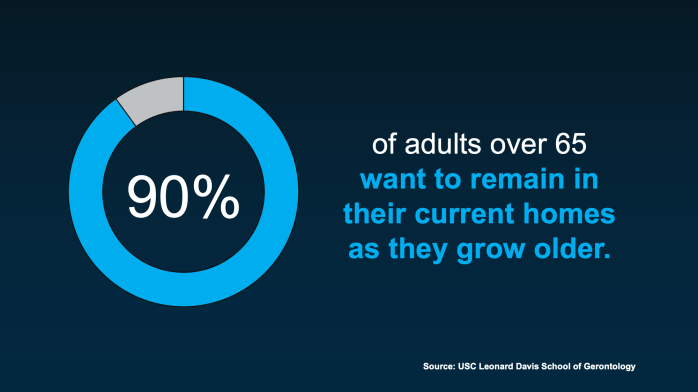

The USC Leonard Davis School of Gerontology found that about 90% of adults over 65 prefer to stay in their homes as they get older (see below):

But even if staying feels like the right answer, it’s still worth thinking ahead about what that might actually look like. That’s where the right agent can really help.

What You Need To Plan for If You’re Staying in Your Home

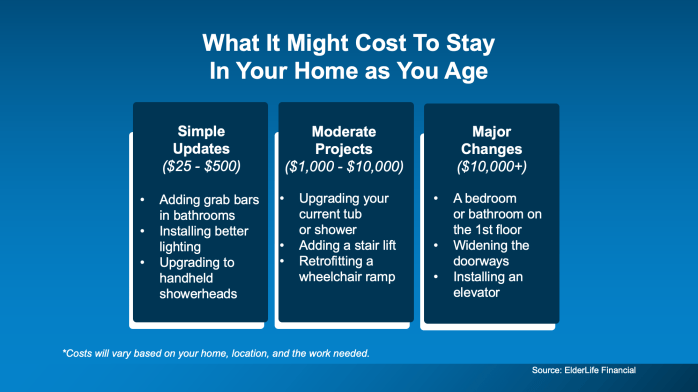

Aging in place is definitely possible. But it’s better if you have a plan. And here’s why. The home that once worked perfectly may need to change with you over the years. And it’s easier if you can anticipate those expenses.

- Sometimes that means small updates: like adding grab bars in the shower.

- Other times, you’ll have to make bigger decisions: like reworking layouts or moving key spaces to the first floor.

Some of those changes are going to be simple. Others can be a meaningful investment. And that’s why thinking about it early matters. Not because you need to decide anything right now, but because it gives you time.

- Time to understand what your home may need.

- Time to explore your options.

- Time to find the right contractors.

- Time to space out the expense of the upgrades.

According to ElderLife Financial, here’s a rough baseline of what it could cost depending on what needs to be done (see below):

And don’t worry. If your heart is really set on staying, but the costs feel like a concern, it helps to know you have options. Depending on your situation, there may be financial assistance programs available, along with tools like home warranties to help manage unexpected costs.

Just remember, if you’re thinking about making updates, it’s always worth having a quick conversation before you start. A real estate agent can help you understand which changes tend to make sense for your situation and how they may impact your home’s value based on your local market.

When Moving Might Make More Sense

But staying isn’t always the best fit for every situation. According to Pegasus Senior Living:

“While most seniors hope to age in place, practical considerations sometimes make selling a home the wiser choice.”

Sometimes, it comes down to a simple shift: when the home that once made life easier starts to make it harder.

That might look like:

- Maintenance or yardwork that’s starting to feel overwhelming

- Stairs or layouts that are getting harder to manage day-to-day

- Or needing more support or care, or being too far from loved ones

And sometimes, it’s not about necessity at all. It’s about lifestyle. Some homeowners just don’t want to live through major renovations. Others are ready to simplify, downsize, or move somewhere that better fits this next chapter, whether that’s a smaller home, a 55+ community, or a place closer to family.

For them, moving simply means making daily life easier.

Bottom Line

There’s no one-size-fits-all answer here.

Some people stay and make updates. Others move to simplify things. Either can be the right choice. The goal isn’t to pick one today. It’s to understand your options early, so when the time comes, you feel confident instead of rushed.

And if you ever want a sounding board to think through what the future could look like for you, let’s connect.

What sets Crawford County apart from other Northern Michigan counties…

Exploring the lifestyle, natural beauty, and real estate opportunities in Northern Michigan

For many people dreaming of living “Up North,” Crawford County, Michigan, quickly rises to the top of the list. With miles of pristine rivers, endless forest trails, and a welcoming small-town community, it offers a lifestyle that feels both peaceful and adventurous at the same time.

Whether someone is looking for a permanent residence, a second home, or an investment property, Crawford County continues to attract buyers who want more space, more nature, and a slower pace of life.

Here are some of the biggest reasons people are making the move.

1. A Lifestyle Built Around the Outdoors

One of the biggest draws to Crawford County is the access to outdoor recreation in every season.

The area is home to thousands of acres of state forest, making it a paradise for people who enjoy:

- Snowmobiling and cross-country skiing in winter.

- Hunting and wildlife viewing.

- Hiking and ORV trail riding.

- Camping and exploring Michigan’s northern wilderness.

The Au Sable River, which runs through Grayling and the surrounding communities, is widely known as one of the premier trout fishing rivers in the Midwest. This kind of access to nature is something many buyers simply can’t find in more populated areas.

For those relocating from cities, the ability to step outside and immediately enjoy Michigan’s outdoors is a major quality-of-life upgrade.

2. A True “Up North” Community

Crawford County offers something many larger areas have lost: a strong sense of community.

The county has a population of just over 13,000 residents, which allows neighbors to know each other and local businesses to feel personal.

Residents often mention that life here feels more connected and intentional. Community events, local festivals, and outdoor gatherings bring people together throughout the year.

Towns like Grayling and Frederic serve as community hubs where small businesses, local restaurants, and family-owned shops are part of everyday life.

3. Affordability Compared to Other Northern Michigan Destinations

Another reason buyers are turning to Crawford County is affordability compared to many other Northern Michigan markets.

According to recent housing data:

- The median home sale price in Crawford County is around $175,000, up about 6% year-over-year.

- Some market reports show a median listing price of around $149,500, depending on property type and timeframe.

- The county’s median home value is roughly $171,974, with an average home value above $215,000.

Compared to many waterfront or resort markets in Northern Michigan, this makes Crawford County a relatively accessible entry point for buyers looking for cabins, recreational property, or year-round homes.

For buyers priced out of larger tourist areas like Traverse City, the region offers similar outdoor beauty at a much more approachable price point.

4. A Market That Still Offers Opportunity

The local housing market currently provides opportunities for both buyers and sellers.

Recent market insights show:

- Roughly 200+ homes are available across the county.

- Homes typically sell within about 47–86 days on the market, depending on the report and time period.

- The area is leaning toward a buyer-balanced market, meaning inventory and demand are closer to equilibrium.

For buyers, this means there may be more choices and negotiating room than in extremely competitive markets.

For sellers, properties that are well-priced and properly marketed can still attract strong interest, particularly if they offer acreage, waterfront access, or proximity to recreation.

5. Ideal for Second Homes, Cabins, and Remote Work

As remote work continues to change where people choose to live, Crawford County has become especially appealing.

Many buyers are searching for:

- Weekend cabins or hunting properties

- Short-term rental investments.

- Vacation homes near trails and rivers.

- Full-time homes with a peaceful lifestyle.

- The area’s large number of seasonal homes reflects this trend. Out of roughly 10,400 housing units in the county, more than 4,500 are considered vacant or seasonal properties, highlighting the popularity of vacation ownership in the region.

6. The Perfect Balance of Nature and Convenience

While Crawford County offers a remote feel, it still provides convenient access to larger cities.

Residents are within driving distance of:

- Gaylord

- Traverse City

- Houghton Lake

- Petoskey

This allows people to enjoy quiet Northern Michigan living while still having access to shopping, dining, healthcare, and regional airports.

The Bottom Line

Crawford County offers something that many people are searching for right now: space, nature, affordability, and community.

With home prices that remain relatively accessible and a lifestyle centered around outdoor recreation, it’s easy to see why more buyers are exploring this part of Northern Michigan.

Whether someone is dreaming of a quiet riverfront cabin, a hunting property in the woods, or a full-time home surrounded by nature, Crawford County continues to be one of Michigan’s hidden gems.

✅ Thinking about buying or selling property in Crawford County?

Working with a local expert who understands the market, the lakes, and the unique lifestyle of Northern Michigan can make all the difference.

Let’s chat! 517.643.1834

The Price You Set Can Make (or Break) Your Sale

There’s one decision you’re going to make when you sell that determines whether your house sells quickly or it sits. Whether buyers make an offer or scroll past it. Whether you walk away with the maximum return, or you end up cutting the price later.

And that’s your asking price.

The #1 Mistake Sellers Make Today: Trusting the Wrong Number

If you’re thinking of moving and trying to figure out what your house may sell for, it’s tempting to start with an online home value tool. They’re fast, free, and easy. And you don’t have to talk to anyone. But here’s the problem: they don’t know your house.

And that can be a bigger drawback than you realize.

Where Online Estimates Fall Short

Online tools often lag behind the market. They look in the rearview mirror, relying on closed sales and delayed information. And in that sense, they’re using incomplete data.

That’s not a miss in how these systems are built. Some information just isn’t available online. Bankrate explains:

“While these tools can be a useful starting point, keep in mind that they typically do not provide the most accurate pricing. Algorithms can only rely on the information available; they can’t account for things like a home’s condition or renovations made since the last public information was updated.”

They can’t see:

- The unique features that make your house special

- All the work you’ve put in to keep it in good condition

- Or, how in-demand your specific neighborhood is right now

So, while they may do a good job in some cases, they can’t be as accurate as a local agent who has boots on the ground day in and day out.

In a market where buyers have more options, a seemingly small margin of error can cost you thousands if you price too low, or weeks of lost momentum and time if you price too high.

If you want to sell for the most money and in the least amount of time, you don’t want the fast answer on how to price your house. You want the right one.

That’s why the savviest homeowners today don’t rely on algorithms when it actually matters. They rely on people, specifically trusted local agents.

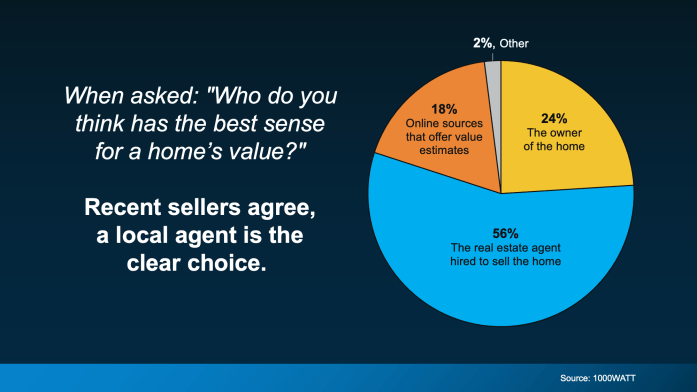

What an Expert Agent Brings to the Table

According to 1000WATT, sellers overwhelmingly believe real estate agents have the best sense of a home’s true value, far more than any automated tools.

That confidence isn’t accidental. As Bankrate puts it:

“A professional appraiser or real estate agent can visit the home in person, assess the neighborhood as a whole as well as the individual property, perform more thorough market research, and consider subjective details.”

And those details matter. A skilled local agent doesn’t just pull reports. They know what’s happening right now:

- What buyers are paying this month, not last month, or even last year

- How does your home compare to the current competition in your neighborhood

- Which features add value based on what buyers are willing to pay for today

- How to price your house to create urgency in this market

And once an agent sets foot in your house, they may even find your online estimate undershot your value. So, if you stick with the estimate you got online, you’d actually be leaving money on the table. And no one wants that.

Bottom Line

While online tools can give you a rough starting point, only a local expert can give you a price that actually works. If you want to know the right number for your house, not just the easiest one to find, let’s talk.

517-643-1834 | morgan@morganrobinson.org

Mortgage Rates Recently Hit a 3-Year Low. Here’s Why That’s Still a Big Deal.

If you’re one of the thousands of homebuyers waiting for rates to fall, you should know it’s already happening. And they recently crossed an important milestone. Rates officially dipped their toes into the 5s – something that hasn’t happened in about 3 years.

This moment marked a critical threshold. Now, rates are sitting in the low 6% territory. And expert forecasts project they’ll hover near this range throughout the year.

Here’s why that’s so good for you.

Why Current Rates Are Such a Big Deal

A mortgage rate doesn’t just affect the interest you end up paying on your home loan. It shapes your entire buying experience.

When rates were up around 7% just one year ago, a lot of buyers felt priced out. Payments were higher. Budgets felt tighter. Affordability was a bigger challenge. That’s especially true for first-time homebuyers, who felt the biggest pinch.

But according to industry experts, that’s starting to change now that rates are slowly inching down. Let’s break down why.

Right now, borrowing costs are in their lowest range in almost 3 years. And that can change the type of home you can afford.

At 6% or below, you’ll see:

- Lower monthly payments. The payment on a $400k home loan is down over $300 compared to when rates were around 7%.

- More buying power, thanks to the extra breathing room in your budget.

In other words, you can now make a stronger offer, purchase in a different location, or buy a home that checks more of your boxes. And that feels like a big shift compared to when rates were at 7%.

This Opens the Door for 550,000 Buyers

To drive home just how much this helps potential homebuyers like you, consider this research from the National Association of Realtors (NAR). It shows that when mortgage rates sit around this level, millions more households can afford a home. When rates are at 6% or below:

- 5.5 million more households can afford the median-priced home

- And roughly 550,000 of those people will likely buy a home within 12 to 18 months

That’s not just speculation. That’s pent-up demand finally getting the green light they’ve been waiting for. You’ve got the chance right now to get ahead and buy before more people notice the game has just changed.

Because whether rates stay in the low 6s or dip back down into the upper 5s, the math is already working in your favor. And the difference from a low 6% to a high 5% isn’t as big as you may think. But the difference from 7% to 6%? That is very much a big deal, and it’s a number that’s already working in your favor.

An Important Call Out

Mortgage rates don’t operate in a vacuum. Home prices, local inventory, property taxes, home insurance, and your personal finances still matter.

And a rate in this territory doesn’t mean every home suddenly works for every buyer. That’s why getting pre-approved and running your numbers with a trusted lender is key.

Still, this rate environment puts more buyers in play than we’ve seen in years. So, if buying didn’t work for you before, it’s worth taking another look.

Bottom Line

Mortgage rates dropping to a 3-year low isn’t just a headline.

For many buyers, where rates are now could be the difference between watching from the sidelines and finally getting the keys to their next home.

If you’ve been waiting for a sign to re-run your numbers and see what’s possible now, this is it.

Let’s take a look at what today’s rates mean for your budget and your buying options.

Contact Me Today! 517-643-1834

Thank You for an Incredible Year — Looking Ahead to 2026 with Optimism

As this year comes to a close, I want to take a moment to say thank you.

Thank you to my clients, friends, referral partners, and community for the trust, support, and encouragement you’ve shown throughout the year. Being part of so many important milestones—new beginnings, fresh starts, and major life changes—has been incredibly rewarding. The successes we experienced this year were only possible because of the people who believed in me and in NextHome Up North.

Together, we navigated a market that required patience, strategy, and clear communication. We celebrated wins, solved challenges, and helped many individuals and families move forward with confidence. I’m proud of what we accomplished and grateful to work alongside a brokerage that truly puts people first.

Looking ahead, I’m genuinely excited about what 2026 has in store.

If a move is on your radar for 2026, there’s a lot more working in your favor than there has been in a while. After a stretch where many people felt stuck, the coming year is shaping up to bring more balance, more options, and more clarity for buyers and sellers alike. Not because the market will suddenly be “easy,” but because key conditions are finally shifting.

Experts agree that improvement is on the horizon. Danielle Hale, Chief Economist at Realtor.com, shares:

“After a challenging period for buyers, sellers and renters, 2026 should offer a welcome, if modest, step toward a healthier housing market.”

The National Association of Realtors echoes that optimism, stating:

“Top economists have one word to sum up the housing market for 2026: opportunity. Lower mortgage rates and a rising supply of homes are expected to open up the housing market… something the real estate industry and potential home buyers and sellers have been waiting for.”

That sense of opportunity is exactly why I’m so excited to serve you in the year ahead. Whether you’re thinking about buying, selling, or simply exploring your options, 2026 may offer the flexibility and confidence many have been waiting for.

Thank you again for being part of my journey this year. I look forward to continuing to serve your real estate needs in 2026—and helping you take the next step when the time is right.

Living Out #HumansOverHouses — A Personal Reflection from Morgan Robinson at NextHome Up North

When I think about what makes NextHome Up North truly special, it’s not the transactions, the market stats, or even the homes themselves — it’s the people. It’s the clients who trust us with their biggest life decisions, the communities that embrace us, and the ways our team shows up not just as agents, but as neighbors, friends, and advocates.

This year has been a powerful reminder of why I love being part of this organization. Our #HumansOverHouses mantra isn’t just a phrase we use in marketing — it’s something we live every day through real, meaningful community involvement. It’s about reaching beyond our roles as real estate professionals to make a tangible impact where we live and work.

In 2025, our office officially tracked an inspiring 110 acts of community service, sponsorships, donations, and volunteer efforts — and that number only scratches the surface of what our team truly gave back. Behind every one of those acts were moments of connection, care, and joy. From fundraising and food drives to supporting local events and lending a hand wherever we saw need, these were not tasks on a checklist — they were expressions of heart.

This team truly embodies what it means to put people first. We’ve helped neighbors through transitions, stood alongside local nonprofits, and showed up for families, schools, events, and initiatives that make our community stronger. And the beauty of it is that many of our efforts weren’t measured solely by numbers — they were measured by the smiles, the gratitude, and the connections formed along the way.

What fills me with pride isn’t just the quantity of service — it’s the quality of care and intention behind each effort. That’s the heartbeat of NextHome Up North — a group of real estate professionals who see every opportunity to give back as a chance to live out our values in service to others.

In addition to this, I had the pleasure of helping 43 individuals & families achieve their real estate goals, totaling over $6.7 million in sales. To simply say I am grateful for each & every client seems to fall short of what I feel in my heart, yet that is what I need to say! Because what a pleasure it is to serve people during one of the largest transactions they will ever make & to have so many amazing folks put their trust in me, many of them, repeat clients. It means the world to me.

So, to my clients: thank you for trusting me with your stories and your dreams.

And to my teammates: thank you for leading with kindness, generosity, and unwavering commitment every single day. I’m proud to be part of a brokerage that measures success in service as much as in sales, and that always remembers that humans — far more than houses — are at the center of everything we do.

— Morgan Robinson, NextHome Up North

Is January the Best Time To Buy a Home?

You may not want to put your homebuying plans into hibernation mode this winter. While a lot of people assume spring is the ideal time to buy a house, new data shows January may actually be the best time of year for budget-conscious buyers.

Kind of surprising, right? Here’s why January deserves a serious look.

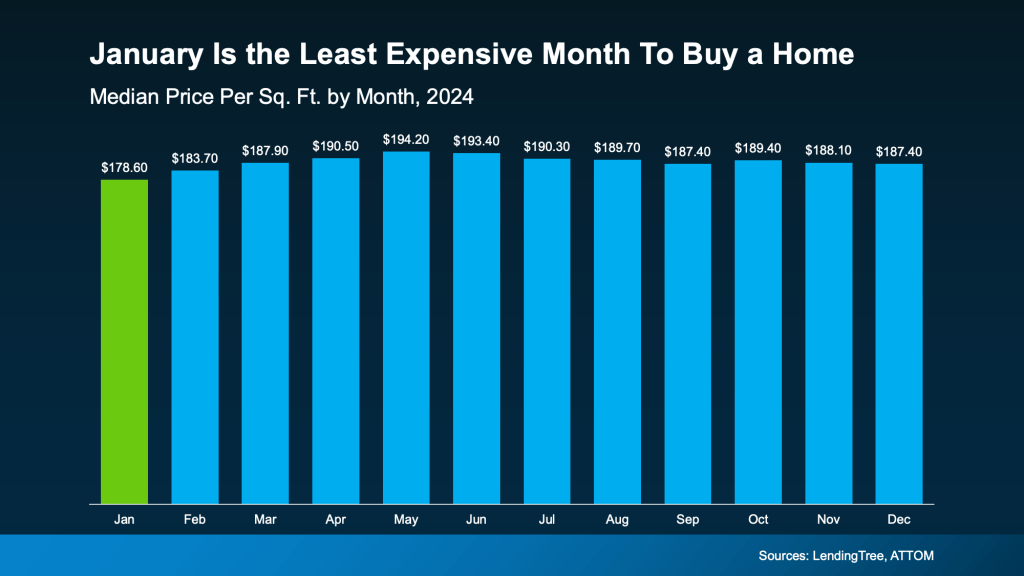

1. Prices Tend To Be Lower This Time of Year

Lending Tree says January is the least expensive month to buy a home. And there’s something to that. January has historically offered one of the lowest price-per-square-foot points of the entire year. But the spring? That’s when demand (and prices) usually peak. And that’s not speculation – it’s a well-known trend based on years of market data.

So, how much less are we talking? Here’s a look at the numbers. According to the last full year of data, for the typical 1,500 square foot house, buyers who closed on their home in January paid around $23,000 less compared to those who bought in May. And that general trend typically holds true each year (see chart below):

Now, your number is going to depend on the price, size, and type of the home you’re buying. But the trend is clear. For today’s buyers, it’s meaningful savings, especially when affordability is still tight for so many households.

2. Fewer Buyers and More Motivated Sellers

And why do buyers typically save in the winter? It’s simple. Winter is one of the slowest times in the housing market each year. Both buyers and sellers tend to pull back, thinking it’s better to wait until spring. And that means:

- You face less competition

- You’re less likely to get into a multiple offer scenario

- Sellers are more willing to negotiate (since there aren’t as many buyers)

With fewer buyers in the market, you can take your time browsing.

But winter doesn’t just thin out the pool of buyers; it also reveals which sellers truly need to sell. Because fewer people are house hunting during the colder months, sellers who really need to move tend to be more open to negotiating. As Realtor.com explains:

“Less competition means fewer bidding wars and more power to negotiate the extras that add up: closing cost credits, home warranties, even repair concessions. . . these concessions can end up knocking thousands of dollars off the price of a home.”

This can include everything from price cuts to covering closing costs, adjusting timelines, and more. It doesn’t mean you’ll automatically get discounts on every home. But it does mean you’re more likely to be taken seriously and given room to negotiate.

Should You Wait for Spring?

Here’s the real takeaway. When you remove the pressure and frenzy that come with the busy spring season, it becomes much easier to get the home you want at a price that fits your budget.

But if you wait until spring, more buyers will be in the market. So, waiting could actually mean you spend more, and you’d have to deal with more stress.

Now, only you can decide the right timing for your life, but don’t assume you should wait for warmer weather before you move.

Buying in January gives you: less competition, potentially lower prices, and more motivated sellers. And those are three perks you’re not going to see if you wait until spring.

Bottom Line

If you’ve been thinking about taking the next step, this season might give you more opportunity than you think.

Curious what buying in January could look like for you? Let’s take a closer look at your numbers and the homes that are available in our area. Contact me today! (517) 643-1834

Buyers Have More Negotiation Power – Here’s How To Use It

You may have heard there are more homes for sale right now. And while that’ll vary depending on the market, it means that overall, things are starting to lean in a more balanced direction. As that happens, some sellers are a bit more open to compromise. Here’s what that means for you.

You may be regaining some negotiating power. That can translate into savings, perks, or even better terms on your purchase – if you know what levers to pull during negotiation.

Why an Agent Is an Essential Part of the Negotiation Process

The complicated part is knowing what is and isn’t on the table. That’s where your agent comes in. According to the National Association of Realtors (NAR), besides finding the right home, the top thing buyers want from their agent is help negotiating the terms of the sale, followed by negotiating the price.

Here’s why. Agents are skilled negotiators and are trained for moments like this. Since your agent is an expert on the local market, they’ll also know what’s working for other buyers (and what’s not), which can help you better understand what’s realistic to ask for.

What’s on the Negotiation Table?

Here are some of the most common concessions an agent can help you negotiate:

- Sale Price: The most obvious concession is the price of the home. And that lever is being pulled more often today. Buyers don’t want to overpay when affordability is already so tight. And sellers who aren’t realistic about their asking price may have to consider adjusting their price.

- Closing Costs: Closing costs are usually about 2-5% of a home’s purchase price and include fees for things like the appraisal, title insurance, and underwriting of your loan. To offset the cash you have to bring to the table, you can ask the seller to pay for some or all of these expenses. This was the most common concession sellers made in 2024, according to NAR.

- Home Warranties: If you’re worried about the maintenance costs that may pop up after you get the keys, you can ask the seller to pay for a home warranty. Since this concession usually isn’t terribly expensive for the seller, it can be a good negotiation tool for a buyer. It’s not a big cost for them, but it can be a big perk for you.

- Home Repairs: Based on the inspection, you’re within your rights to ask the seller to make repairs. If the seller doesn’t want to, they could offer to drop the home price or cover some closing costs, so you have more room in your budget to take care of the repairs yourself.

- Fixtures: Want that washer and dryer to stay? Maybe the stainless-steel fridge, too? In many cases, you can ask for appliances or even furniture to be included in the deal, which will save you money when you move in.

- Closing Date: The closing date is also negotiable. Based on your timeline, you may also request a faster or extended closing window. Depending on the seller’s needs, this could be great for their situation, too.