People Are Still Moving, Even with Today’s Affordability Challenges

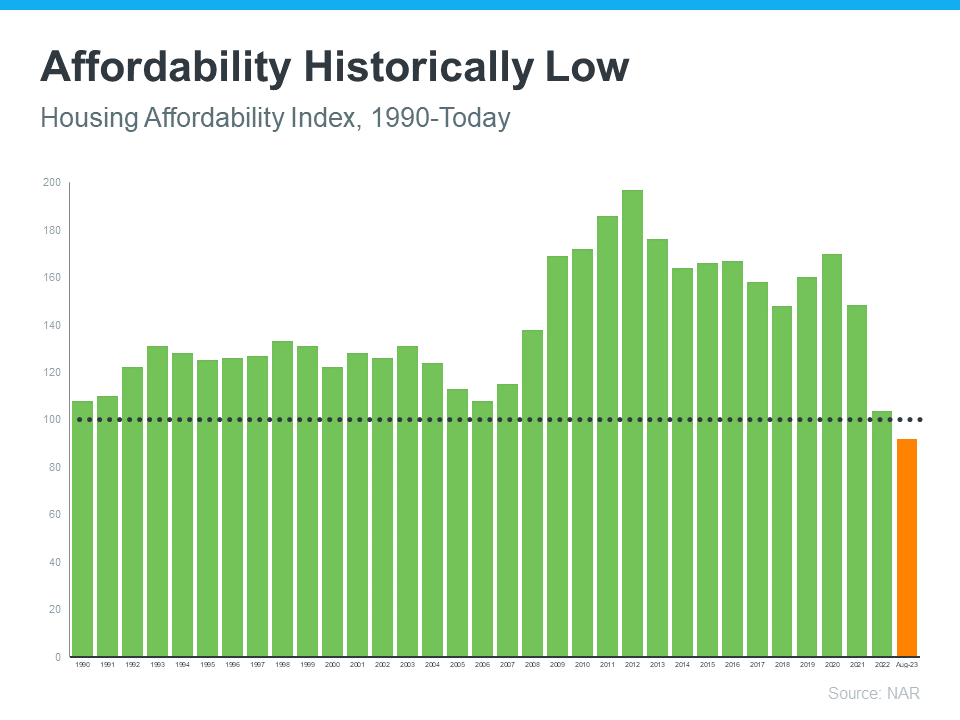

If you’re thinking about buying or selling a home, you might have heard that it’s tough right now because mortgage rates are higher than they’ve been over the past few years, and home prices are rising. That much is true. Take a look at the graph below. It breaks down how the current affordability situation stacks up to recent years.

The National Association of Realtors (NAR) explains how to read the values on the graph:

“To interpret the indices, a value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home.”

The black dotted line represents that 100 value on the index. Essentially, the higher the bar, the more affordable homes are. As you can see, the orange bar for today shows higher mortgage rates and home prices have created a clear challenge. But, while affordability is definitely tighter right now, that doesn’t mean the housing market is at a standstill.

According to NAR, based on the pace of sales right now, just under 4 million homes will sell this year. With some simple math, let’s break down what that really means for you:

- 3.96 million homes divided by 365 days in a year = 10,849 houses sell each day

- 10,849 divided by 24 hours in a day = 452 houses sell per hour

- 452 divided by 60 minutes in an hour = about 8 houses sell each minute

So, on average, over 10,000 homes sell each day in this country. Whether you’re a buyer or a seller, this goes to show there are still ways to make your move possible, even at a time when affordability is tight.

An Agent Can Help You Make Your Move a Reality

You may be wondering how other homebuyers and sellers are making this happen now. One of the biggest game-changers in today’s market is working with a trusted local real estate agent. Great agents are helping other people just like you navigate today’s market and the current affordability situation, and their insight is invaluable right now.

True professionals will be able to offer advice tailored to your specific wants, needs, budget, and more. Not to mention, they’ll also be able to draw on their experience of what’s working for other buyers and sellers right now. This could mean broadening your search, if needed, to include other housing types like condos, townhouses, or neighborhoods a bit further out to help offset some of the affordability challenges today.

Bottom Line

You might think there aren’t many people buying or selling homes right now since affordability is tighter than it’s been in quite some time, but that’s not the case. It’s true that buying a home has become more expensive over the past couple of years, but people are still moving.

If you’re hoping to buy or sell a home today, know that other people are still making their goals a reality – and that’s happening in large part because of the help and advice of skilled local real estate agents. Want to talk to a trusted professional about your own move? Let’s connect.

A Real Estate Agent Helps Take the Fear Out of the Market

Do negative headlines and talk on social media have you feeling worried about the housing market? Maybe you’ve even seen or heard something lately that scares you and makes you wonder if you should still buy or sell a home right now.

Regrettably, when news in the media isn’t easy to understand, it can make people feel scared and unsure. Similarly, negative talk on social media spreads fast and creates fear. As Jason Lewris, Co-Founder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

But it doesn’t have to be that way. Buying a home is a big decision, and it should be one you feel confident making. You should lean on a trusted real estate agent to help you separate fact from fiction and get the answers you need.

That agent will use their knowledge of what’s really happening with home prices, housing supply, expert forecasts, and more to give you the best possible advice. The National Association of Realtors (NAR) explains:

“. . . agents combat uncertainty and fear with a combination of historical perspective, training and facts.”

The right agent will help you figure out what’s going on at the national level and in your local area.

They’ll debunk headlines using data you can trust. Plus, they have in-depth knowledge of the industry and can provide context, so you know how current trends compare to the normal ebbs and flows in the housing market, historical data, and more.

Then, to make sure you have the full picture, an agent can tell you if your local area is following the national trend or if they’re seeing something different in your market. Together, you can use all that information to make the best possible decision.

After all, making a move is a potentially life-changing milestone. It should be something you feel ready for and excited about. And that’s where a trusted expert comes in.

Bottom Line

If you need reliable information about the housing market and expert advice about your own move, let’s connect.

Why You May Still Want To Sell Your House After All

Even though you may feel reluctant to sell your house because you don’t want to take on a mortgage rate that’s higher than the one you have now, there’s more to consider. While the financial side of things does matter, your personal needs may actually matter just as much. As an article from Bankrate says:

“Deciding whether it’s the right time to sell your home is a very personal decision. There are numerous important questions to consider, both financial and lifestyle-based, before putting your home on the market.”

So, ask yourself this: Why did I want to move in the first place?

Chances are your primary motivation wasn’t just financial in nature. Why you’re really thinking about selling likely has more to do with something changing in your life or a shift in what you need out of your house.

Reasons Homeowners Still Need To Sell Today

Let’s explore some of the most common reasons sellers are moving today. A recent article from Builder Online helps shed light on this. In this research, they identified the following categories:

- Marriage – If you just got married, you may find you either need more space than you currently have, or the two of you want to find a new place you picked out together.

- Divorce – If you’re getting separated or are divorcing your partner, chances are it’ll be difficult to live under the same roof. Selling the place you have, so you can own get your own spot, may be necessary.

- Births – If your household is growing, you may need more square footage, including more bedrooms. If you’re running out of room for everyone, you may not be able to wait to move.

- Deaths – If you’ve recently lost a loved one, it can be hard to spend time in that home. You may need to move for financial reasons or because you no longer need all the space.

- Retirement – If you’re in the process of retiring, or you just did, you may be looking to downsize to cut costs, relocate to be closer to loved ones, or move to a dream location. In this new phase of life, your current home may not be able to deliver what you need.

You may find you share one of these top motivators. If any of these resonate with you, it may be time to move so you can find a house better suited to your changing needs. A survey from Realtor.com finds other sellers are in the same boat. It says, 1 in 4 sellers are choosing to move for personal reasons, even with current mortgage rates:

“. . . more than half of seller-buyers (56%) who are planning to sell in the next 12 months said they are waiting for rates to come down, while 25% need to sell soon for personal reasons.”

If you need to sell now because something in your own life has changed, don’t let rates hold you back from what you want. You have options to help make that move possible. You can use the equity you already have in your current home toward your next purchase. And with how much equity homeowners have right now, you may be able to finance less than you’d expect or pay all cash to avoid borrowing at all.

Bottom Line

When you’re ready to prioritize your changing needs, let’s connect. You need an expert on your side to help you list your house and find a home that delivers everything you’re looking for.

Don’t Fall for the Next Shocking Headlines About Home Prices

If you’re thinking of buying or selling a home, one of the biggest questions you have right now is probably: what’s happening with home prices? And it’s no surprise you don’t have the clarity you need on that topic. Part of the issue is how headlines are talking about prices.

They’re basing their negative news by comparing current stats to the last few years. But you can’t compare this year to the ‘unicorn’ years (when home prices reached record highs that were unsustainable). And as prices begin to normalize now, they’re talking about it like it’s a bad thing and making people fear what’s next. What we’re starting to see now is the return to more normal home price appreciation.

To help make home price trends easier to understand, let’s focus on what’s typical for the market and omit the last few years since they were anomalies.

Let’s start by talking about seasonality in real estate. In the housing market, there are predictable ebbs and flows that happen each year. Spring is the peak homebuying season when the market is most active. That activity is typically still intense in the summer but begins to wane as the cooler months approach. Home prices follow along with seasonality because prices appreciate most when something is in high demand.

That’s why, before the abnormal years we just experienced, there was a reliable long-term home price trend. The graph below uses data from Case-Shiller to show typical monthly home price movement from 1973 through 2021 (not adjusted, so you can see the seasonality):

As the data from the last 48 years shows, at the beginning of the year, home prices grow, but not as much as they do entering the spring and summer markets. That’s because the market is less active in January and February since fewer people move in the cooler months. As the market transitions into the peak homebuying season in the spring, activity ramps up, and home prices go up a lot more in response. Then, as fall and winter approach, activity eases again. Price growth slows, but still typically appreciates.

Why This Is So Important to Understand

In the coming months, as the housing market moves further into a more predictable seasonal rhythm, you’re going to see even more headlines that either get what’s happening with home prices wrong or, at the very least, are misleading. Those headlines might use a number of price terms, like:

- Appreciation: when prices increase.

- Deceleration of appreciation: when prices continue to appreciate, but at a slower or more moderate pace.

- Depreciation: when prices decrease.

They’re going to mistake the slowing home price growth (deceleration of appreciation) that’s typical of market seasonality in the fall and winter and think prices are falling (depreciation). Don’t let those headlines confuse you or spark fear. Instead, remember it’s normal to see a deceleration of appreciation, slowing home price growth, as the months go by.

Bottom Line

If you have questions about what’s happening with home prices in our local area, let’s connect.

Why Buying or Selling a Home Helps the Economy and Your Community

If you’re thinking about buying or selling a house, it’s important to know that it doesn’t just affect your life, but also your community.

The National Association of Realtors (NAR) releases a report every year to show how much economic activity is generated by home sales. The chart below illustrates that impact:

As the visual shows, when a house is sold, it can make a big difference in the local economy. The impact comes largely from the workers required to build, update, and buy and sell homes. Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), explains how the housing industry adds jobs to a community:

“The economic impact means housing is a significant job creator. In fact, for every single-family home built, enough economic activity is generated to sustain three full-time jobs for a year, per NAHB research. . . . And one job for every $100,000 in remodeling spending.”

Housing being a major job creator makes sense when you consider there are many different industries involved in the process. A recent article from Fortune notes housing activity could have a more robust impact than you think due to the many ways it’s tied to the economy:

“Housing has three direct linkages to economic activity (GDP): the construction of new homes, the remodeling of existing homes, and that of housing transactions. . . . consider the activity associated with home sales – think broker fees, lawyers, etc. – which are a sizable contributor to housing’s GDP footprint.”

When you buy or sell a home, you work with a team of professionals, including contractors, specialists, lawyers, and city officials. Each person plays a role in making the transaction happen.

So, when you make a move in the housing market, you’re not just meeting your own needs, you’re also making a positive impact on the community. Knowing this can give you a sense of empowerment as you make your decision this year.

Bottom Line

Each and every home sale is important for the local economy. If you’re ready to move, let’s connect. It won’t just change your life – it’ll also have a strong positive effect on the whole community.

The Three Factors Affecting Home Affordability Today

There’s been a lot of focus on higher mortgage rates and how they’re creating affordability challenges for today’s homebuyers. It’s true that rates have climbed since the record-low we saw during the pandemic. But home affordability is based on more than just mortgage rates – it’s determined by a combination of mortgage rates, home prices, and wages.

Considering how each one of these factors is changing gives you the full picture of home affordability today. Here’s the latest.

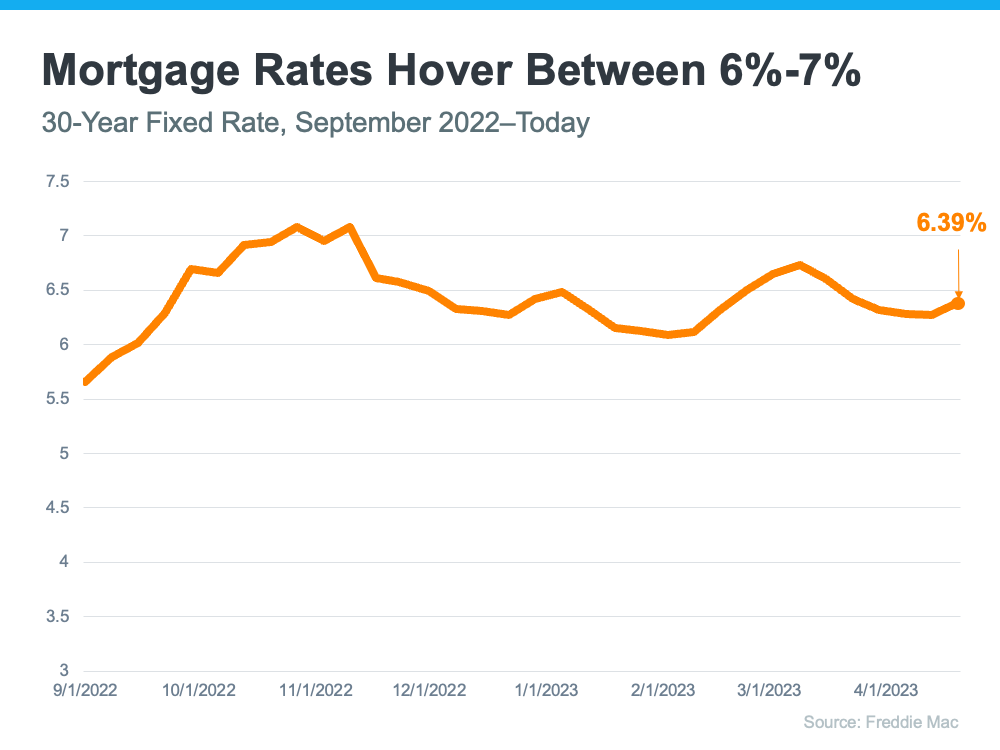

1. Mortgage Rates

While mortgage rates are higher than they were a year ago, they’ve hovered primarily between 6% and 7% for nearly eight months now (see graph below):

As the graph shows, mortgage rates have experienced some volatility during that time. And even a small change in mortgage rates impacts your purchasing power. That’s why it’s so important to lean on your team of real estate professionals for expert advice to stay up to date on what’s happening in the market. While it’s hard to project where mortgage rates will go from here, many experts agree they’ll likely continue to remain around 6%-7% in the immediate future.

2. Home Prices

Over the past few years, home prices appreciated rapidly as the record-low mortgage rates we saw during the pandemic led to a surge in buyer demand. The heightened buyer demand happened while the supply of homes for sale was at record lows, and that imbalance put upward pressure on home prices. However, today’s higher mortgage rates have slowed down price appreciation.

And, the truth is, home price appreciation varies by market. Some areas are seeing slight declines while others have prices that are climbing. As Selma Hepp, Chief Economist at CoreLogic, explains:

“The divergence in home price changes across the U.S. reflects a tale of two housing markets. Declines in the West are due to the tech industry slowdown and a severe lack of affordability after decades of undersupply. The consistent gains in the Southeast and South reflect strong job markets, in-migration patterns and relative affordability due to new home construction.”

To find out what’s happening with prices in your local market, reach out to a trusted real estate agent.

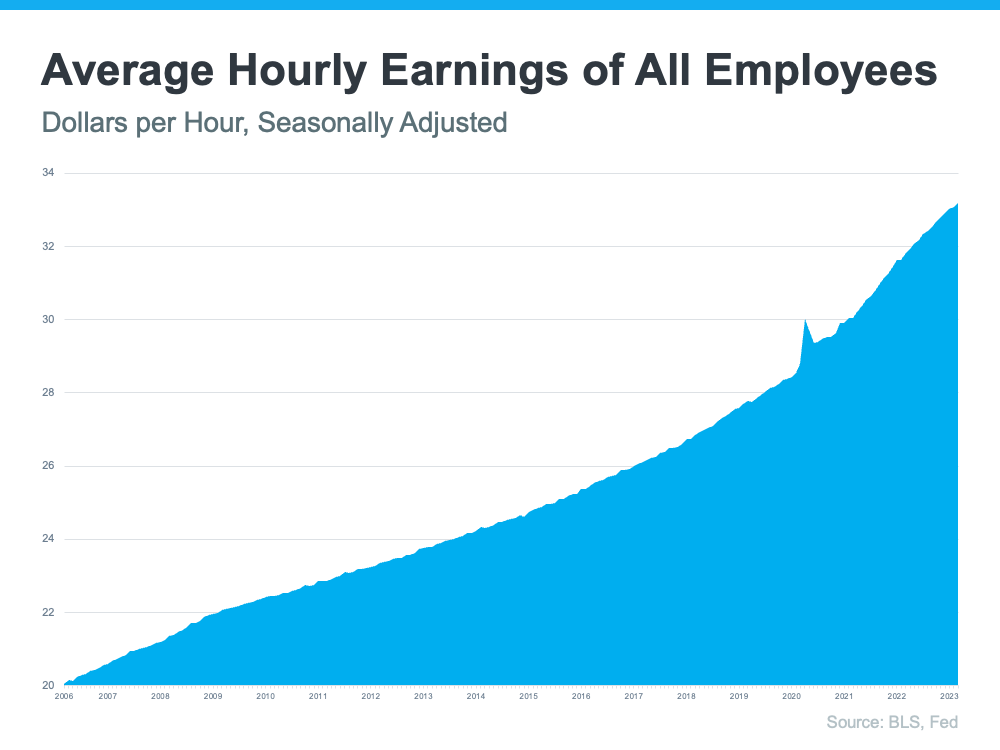

3. Wages

The most positive factor in affordability right now is rising income. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have grown over time:

Higher wages improve affordability because they reduce the percentage of your income it takes to pay your mortgage since you don’t have to put as much of your paycheck toward your monthly housing cost.

Home affordability comes down to a combination of rates, prices, and wages. If you have questions or want to learn more, reach out to a real estate professional who can explain what’s happening locally and how these factors work together.

If you’re planning to buy a home, knowing the key factors that impact affordability is important so you can make an informed decision. To stay up to date on the latest on each, let’s connect today.

Bottom Line

Why Buying a Home Is a Sound Decision

If you’re thinking about buying a home, you want to know if the decision will be a good one. And for many, that means thinking about what home prices are projected to do in the coming years and how that could impact your investment.

This year, we aren’t seeing home prices fall dramatically. As the year goes on, however, some markets may go up in value while others may lose value. That’s why it’s helpful to keep the long-term view in mind. Experts project a return to a steadier rate of price appreciation in the years that follow.

Home Price Appreciation in the Years Ahead

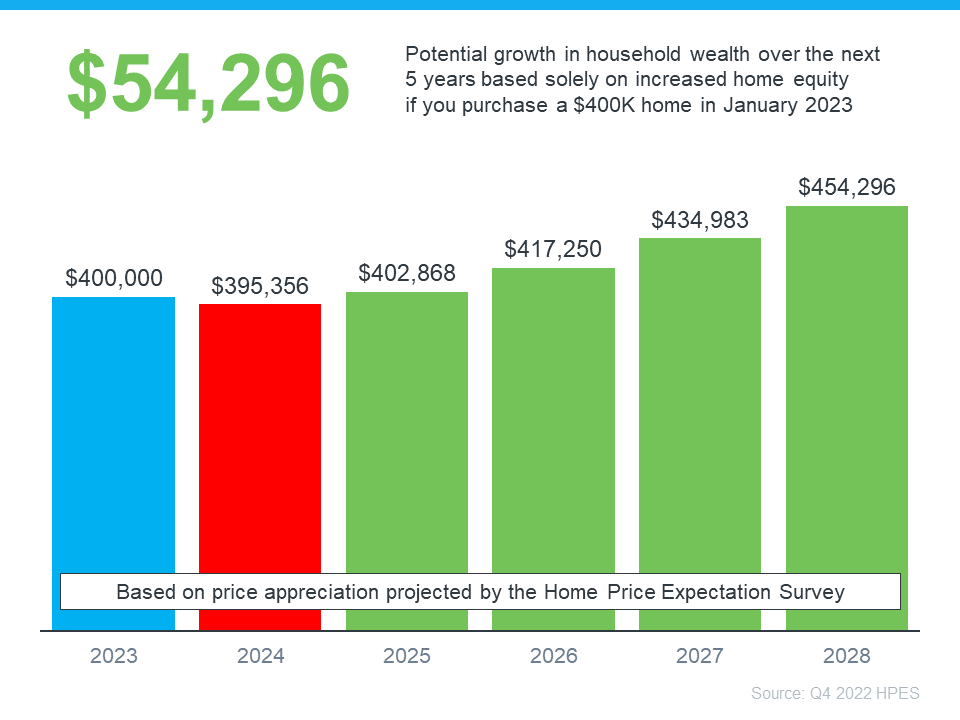

Over 100 economists, investment strategists, and housing market analysts were polled by Pulsenomics in their latest quarterly Home Price Expectation Survey (HPES). The report indicates what they believe will happen with home prices over the next five years. As the graph below shows, after mild depreciation this year, these experts forecast home prices will return to more normal levels of appreciation through 2027.

The big takeaway is experts aren’t forecasting a drastic fall in home prices nationally, even though some markets will see home price appreciation while others may depreciate. And when they look further out, they see steady price appreciation in the long run. That’s a great example of why homeownership wins over time.

What Does This Mean for You?

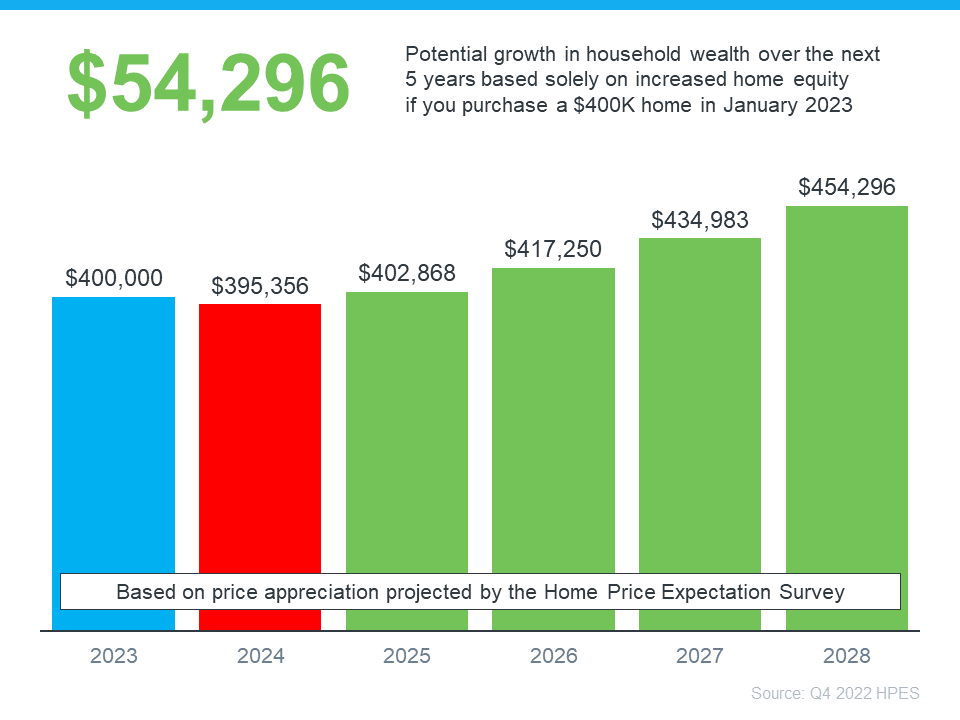

Once you buy a home, price appreciation raises your home’s value, and that grows your household wealth. Here’s how a typical home’s value could change over the next few years using the expert price appreciation projections from the survey mentioned above (see graph below):

Once you buy a home, price appreciation raises your home’s value, and that grows your household wealth. Here’s how a typical home’s value could change over the next few years using the expert price appreciation projections from the survey mentioned above (see graph below):

In this example, if you bought a $400,000 home at the beginning of this year and factor in the forecast from the HPES, you could accumulate over $54,000 in household wealth over the next five years. So, if you’re wondering if buying a home is a sound decision, keep in mind what a strong wealth-building tool it is long term.

Bottom Line

According to the experts, while we may see slight depreciation this year, home prices are expected to grow over the next five years. If you’re ready to become a homeowner, know that buying today can set you up for long-term success as home values (and your own net worth) are projected to grow.

Let’s connect to begin the homebuying process today.

Spring into Action: Boost Your Home’s Curb Appeal with Expert Guidance

To sell your home this spring, it may need more preparation than it would have a year or two ago. Today’s housing market has a different feel. There are more homes for sale than at this time last year, but inventory is still historically low. So, if a house has been sitting on the market for a while, that’s a sign it may not be hitting the mark for potential buyers. But here’s the thing. Right now, homes that are updated and priced at market value are still selling fast.

Today, homes with curb appeal that are presented well are still selling quickly, and sometimes over the asking price. According to Danielle Hale, Chief Economist at realtor.com:

“In a market where costs are still high and buyers can be a little choosier, it makes sense they’re going to really zero in on the homes that are the most appealing.”

With the spring buying season just around the corner, now’s the time to start getting your house ready to sell. And the best way to determine where to spend your time and money is to work with a trusted real estate agent who can help you understand which improvements are most valuable in your local market.

Curb Appeal Wins

One way to prioritize updates that could bring a good return on your investment is to find smaller projects you can do yourself. Little updates that boost your curb appeal usually work well. Investopedia puts it this way:

“Curb-appeal projects make the property look good as soon as prospective buyers arrive. While these projects may not add a considerable amount of monetary value, they will help your home sell faster—and you can do a lot of the work yourself to save money and time.”

Small cosmetic updates, like refreshing some paint and power washing the exterior of your home, create a great first impression for buyers and help it stand out. Work with a real estate professional to find low-cost projects you can tackle around your house that will appeal to buyers in your area.

Not All Updates Are Created Equal

When deciding what you need to do to your house before selling it, remember you’re making these repairs and updates for someone else. Prioritize projects that will help you sell faster or for more money over things that appeal to you as a homeowner.

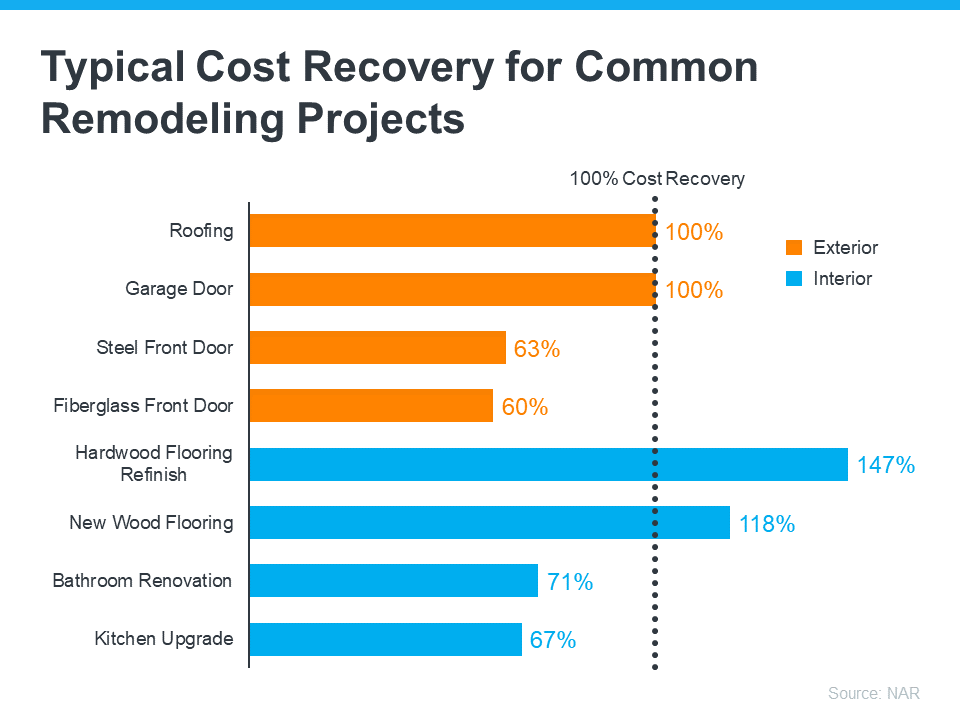

The 2022 Remodeling Impact Report from the National Association of Realtors (NAR) highlights popular home improvements and what sort of return they bring for the investment (see graph below):

Remember to lean on your trusted real estate advisor for the best advice on the updates you should invest in. They’ll know what local buyers are looking for and have the latest insights into what your house needs to sell quickly this spring.

Bottom Line

As we approach the spring season, now’s the time to get your house ready to sell.

Let’s connect today to find out which updates make the most sense.

3 Ways You Can Use Your Home Equity

If you’re a homeowner, odds are your equity has grown significantly over the last few years as home prices skyrocketed and you made your monthly mortgage payments. Home equity builds over time and can help you achieve certain goals. According to the latest Equity Insights Report from CoreLogic, the average borrower with a home loan has almost $300,000 in equity right now.

As you weigh your options, especially in the face of inflation and talk of a recession, it’s important to understand your assets and how you can leverage them. A real estate professional is the best resource to help you understand how much home equity you have and advise you on some of the ways you can use it. Here are a few examples.

1. Buy a Home That Fits Your Needs

If you no longer have the space you need, it might be time to move into a larger home. Or it’s possible you have too much space and need something smaller. No matter the situation, consider using your equity to power a move into a home that fits your changing lifestyle.

If you want to upgrade your house, you can put your equity toward a down payment on the home of your dreams. And if you’re planning to downsize, you may be surprised that your equity may cover some, if not all, of the cost of your next home. A real estate advisor can help you figure out how much equity you have and how you can use it toward the purchase of your next home.

2. Reinvest in Your Current House

According to a recent survey from Point, 39% of homeowners would invest in home improvement projects if they chose to access their equity. This is a great option if you want to change some things about your living space but you aren’t ready to make a move just yet.

Home improvement projects allow you to customize your home to suit your needs and sense of style. Just remember to think ahead with any updates you make, as some renovations add more value to your home and are more likely to appeal to future buyers than others. For example, a report from the National Association of Realtors (NAR) shows refinishing or replacing wood flooring has a high cost recovery. Lean on a local professional for the best advice on which projects to invest in to get the greatest return on your investment when you sell.

3. Pursue Your Personal Goals

In addition to making a move or updating your house, home equity can also help you achieve the life goals you’ve dreamed of. That could mean investing in a new business venture, retiring or downsizing, or funding an education. While you shouldn’t use your equity for unnecessary spending, leveraging it to start a business or putting it toward education costs can help you achieve other lifelong goals.

Bottom Line

Your equity can be a game changer. If you’re unsure how much equity you have in your home, let’s connect so you can start planning your next move.

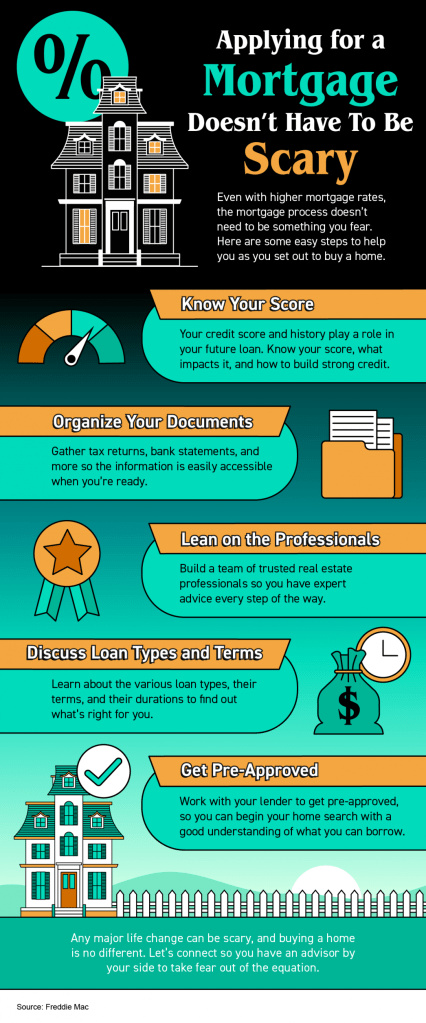

Taking the Fear out of Saving for a Home

If you’re planning to buy a home, knowing what to budget for and how to save may sound scary at first. But it doesn’t have to be. One way to take the fear out of budgeting is to understand some of the costs you might encounter. And to do that, turn to trusted real estate professionals. They can help you plan your finances and prepare your budget.

Here are just a few costs experts say you can expect.

1. Down Payment

Saving for your down payment is likely at top of your mind as you set out to buy a home. But do you know how much you’ll need to save? While each situation is different, there’s a common misconception that putting 20% down toward your purchase is required. An article from the Mortgage Reports explains why that’s not always the case:

“The idea that you have to put 20% down on a house is a myth. . . . The right amount depends on your current savings and your home buying goals.”

To understand your options, partner with a trusted real estate professional to go over the various loan types, down payment assistance programs, and what each one requires.

2. Closing Costs

Make sure you also budget for closing costs, which are a collection of fees and payments made to the various people involved in your transaction. Bankrate explains:

“Closing costs are the fees you pay when finalizing a real estate transaction, whether you’re refinancing a mortgage or buying a new home. These costs can amount to 2 to 5 percent of the mortgage so it’s important to be financially prepared for this expense.”

The best way to understand what you’ll need at the closing table is to work with a trusted lender. They can provide you with answers to the questions you might have.

3. Earnest Money Deposit

If you want to cover all your bases, you can also consider saving for an earnest money deposit (EMD). An EMD is a money you pay as a show of good faith when you make an offer on a house. According to realtor.com, it’s usually between 1% and 2% of the total home price.

This deposit works like a credit. It’s not an added expense – it’s paying a portion of your costs upfront. You’re using some of the money you already saved for your purchase to show the seller you’re committed and serious about their house. Realtor.com describes how it works as part of your sale:

“It tells the real estate seller you’re in earnest as a buyer, . . . . Assuming that all goes well and the buyer’s good-faith offer is accepted by the seller, the earnest money funds go toward the down payment and closing costs. In effect, earnest money is just paying more of the down payment and closing costs upfront.”

Keep in mind, an EMD isn’t required, and it doesn’t guarantee your offer will be accepted. It’s important to work with a real estate advisor to understand what’s best for your situation and any specific requirements in your area. They’ll help you determine what moves you should make in the home-buying process to have the greatest success.

Bottom Line

Budgeting for your home purchase doesn’t have to be scary. Let’s connect so you’ll have an expert on your side to answer any questions you have along the way.

{kind=link}